Part 10 of Illegal Naked Shorting Series: Legal Shorting of Stocks is a Loser’s Game but Illegal Naked Shorting Transforms It into a Winner’s Game

Upfront Caveat

When I launched my research on stock manipulation and the prominent role played by illegal naked shorting, I believed that I had a fair understanding of the subject and could knock out comprehensive research in just a few blogs. However, as I dug in I was taken aback at how complex and widespread this subject is. I think that a team of hundreds of experts with unlimited resources would have difficulty ferreting out all of the details on a scam that Wall Street has been perpetrating and perfecting for over 40 years.

I realized that it would be impossible for one person to execute a comprehensive analysis without making mistakes, omissions and errors. I had two choices. I could just give up or I could resign myself to the inevitability of making mistakes and correcting them as I gained more knowledge. I chose the latter. In my previous blogs and in this one, there are certainly some mistakes and as I become aware of them, I will correct them. However, I strongly believe that my research is broadly accurate in its attempt to show how Wall Street employs illegal naked shorting and associated tactics to routinely manipulate stock prices for many, many, many companies and to line their pockets with what is likely hundreds of billions of dollars each year at the expense of investors and publicly traded companies.

Summary

In my last blog, I discussed the risks and rewards of short selling as compared to buying stocks. It is crystal clear that short selling as a long term investment strategy is extremely unattractive versus buying stocks. It is applicable to only a very limited number of short term trades because of the punishing costs of retaining a short position and unlimited liability if the stock price rises instead of falling. In sharp contrast, since the Buttonwood Agreement of 1792, which presaged the New York Stock Exchange, buying and holding stocks has been shown to be a winner’s game. If carried on as a primary investment strategy over a long period of time, short selling is a loser’s game as short sellers are swimming against the tide of rising stock prices.

The paradox is that short selling is a huge enterprise on Wall Street as carried on by aggressive and often predatory hedge funds. Stock lending to facilitate short selling is a huge and profitable business for the elite Wall Street firms like Goldman Sachs, Morgan Stanley, Merrell Lynch, et al and has been estimated to account for as much as 20% of their net income. I recognize that not all stock lending is associated with short selling as some is attributable to hedging and risk arbitrage, but much of it is.

So how has the losing game of short selling been changed into a winner’s game? I have only empirical evidence, but in my judgment, certain hedge funds have been able to use illegal naked shorting combined with other tactics to make short selling a winner’s game. In many cases hedge funds acting through collaborating market makers can create huge numbers of counterfeit shares that can overwhelm demand. Illegal naked shorting also takes away or reduces a major disadvantage of short selling and that is the borrowing costs.

If you are not actually borrowing shares, there is no actual borrowing cost. However, the hedge fund is not the one creating the counterfeit shares. It is the market makers and they can demand a borrowing cost even if they don’t locate shares to borrow and just create counterfeit shares. This counterfeit borrowing cost is much reduced from what a legitimate locate and borrow would cost. This allows for (illegal) shorts to be maintained for a much longer period of time.

Perspective

The trend of the market has been steadily upward for over 200 years so that buying and holding stocks is a winner’s game in which on balance all investors can win. Conversely, shorting of stocks is betting against house odds and is a loser’s game if shorting is carried on over a long period. To be successful in short selling one has to have a total trading focus, both in regard to the market and individual stocks. Timing must be precise because of the ongoing cost of maintaining a short position and the unlimited liability when the short seller is wrong.

To be a successful short seller, you have to be able to sell high and buy low time after time. This means that you are consistently able to recognize and go against the prevailing psychology of the market in which strong positive sentiment creates higher stock price and pessimism leads to lower prices. Few if any investors have the ability to ignore mass psychology that drives stocks. In addition, the timing has to be exquisite. I don’t consider myself particularly smart, but I do have a lot of experience and knowledge from my forty plus years of working on Wall Street and investing. At times in the past, I have tried to trade in and out of the market by selling high and buying low. I have usually regretted it. .

I have heard many claim that they consistently trade profitably in and out of the market, but I have never met any in my long experience on Wall Street. Indeed, the hedge funds who bill themselves as the smartest people on Wall Street and aggressively trade in and out on both the long and short side have poor records. Statistics from Credit Suisse Hedge Fund Index indicated that from January 1994 to October 2018 – through both bull and bear markets – the passive S&P 500 Index outperformed their hedge fund index by about 2.25 % annually. This suggests that the aggressive short term trading strategies used by hedge funds produce decidedly inferior returns when compared to passive investing in an index fund.

And yet, short selling and the associated business of stock lending is a huge business. Why is that? You probably know by now that I think that both legal shorting in conjunction with illegal naked shorting are extensively used on Wall Street to manipulate stock prices downward and trade around a predictable downward trend in the stock price. This converts the loser’s game of short selling into a highly profitable, low risk investment strategy (scam).

I consistently ask myself whether I am so biased that I am seeing evil where none exists and I am excoriating good honest employees of hedge funds, investment banks and market makers who are performing the outstanding service of reducing volatility, reducing settlement risk and increasing liquidity. I have no data to support my charges because any such data is hidden with the dark confines of the DTCC and inaccessible to the public. I have two things to go on. The first is an overwhelming number of cases I have observed in which I have seen and others have seen inexplicable drops in stock prices that are clearly consistent with market manipulation. The other is that as I have tried to show in prior blogs, the DTCC and its participants can easily use the current clearing and settlement system and ineffective regulations riddled with loopholes to create counterfeit shares and also to hide their trading activity. The DTCC is a self-regulating organization which means that there is no one, including the SEC, who has a good understanding of what they and their member firms are doing.

This blog follows on the last one by looking at the economics that drive various participants in the short selling game.

Borrowing Cost for the Short Seller

A short seller borrows stock from a willing lender and then sells the borrowed stock to a third party. The economics of the trade are dependent on being able to later buy the stock at a lower price and return the borrowed stock to the lender. However, there are meaningful costs associated with the borrowing of stock. The short seller must enter into a loan agreement with the lender agreeing to pay an agreed upon interest rate for a certain period of time. On large liquid stocks, the annualized interest rate can be 5% to 10% with the period of the loan variable depending on the strategy of the short seller. On smaller, less liquid, hard to borrow stocks, annualized interest rates as high as 40% sometimes occur. Particularly in a case like the latter, the cost of borrowing is so high that the short seller has a very small time window of days, weeks or a month or so for the stock to decline sharply.

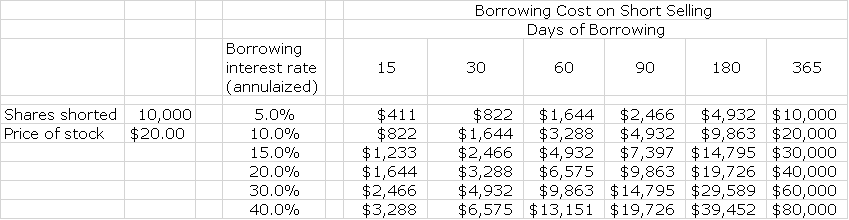

The following table is intended to illustrate how interest expense can vary on short sales. The assumptions used are as follows:

- I arbitrarily assume that a hedge fund manager decides to short 10,000 shares of a stock selling at $20.00.

- They take out a $200,000 loan to cover the cost of the stock that they borrow. I then calculate the interest expense associated with this $200,000 loan at various interest rates ranging from 5% annualized to 40% and for a number of days ranging from a low of 15 days to a high of 365.

- I use this to calculate the interest expense for 36 different combinations of annualized interest rate and days that the loan extends over.

Here is the calculation:

Interest expense = (annualized interest rate) divided by 365 multiplied by (days of borrowing) multiplied by (stock price) multiplied by (number of shares shorted).

Let’s calculate an example in which the 20,000 shares are shorted for 60 days at an annualized rate of 15%.

Interest expense = 15%/365*60*$20*10,000 = $4,932

Here is the table for interest rates ranging from 5% to 40% for periods of borrowing ranging from 15 to 365 days.

In the example in which 10,000 shares are shorted at $20.00 per share the short seller loses 2.5% of their investment ($4,932/ $200,000) in 60 days if they hold the position and the stock price remains unchanged at $20.00. If the position is held for a year with no change in stock price the loss would be $30,000 or 15%. If the Company pays a dividend over the borrowing period, the short seller must pay it to the lender which would add to the loss. Also, if the stock price goes up, the amount of the loan and associated interest expense increases. This shows that successful short selling requires a fairly quick decline in stock price. It is a gambling, not an investment strategy.

Collateral Is Required from the Short Seller

Lenders require that short sellers put up collateral against their loans. In the case of an individual investor or a hedge fund, they must have a margin account to allow for this. The lender who in this case is the nominee brokerage firm that is holding their account would look to other stocks owned outright as collateral. They would require collateral in excess of the amount of money borrowed, probably on the order of 105% to 110% of the loan. If the stock price goes up, more collateral is required. If at some point, the collateral backing the loan increases to a dangerous level relative to the loan and assets in the short seller’s account, some or all of the collateral (stocks in the account) can be liquidated to repay the loan.

Background Information on Clearing and Settlement of Stock Trades that is Useful in Understanding Stock Lending and Illegal Naked Shorting

I have discussed clearing and settlement of stock trading in my previous blogs, but this is such a complicated subject that I am including a brief refresher that will hopefully help you to understand what goes on in stock lending and then in illegal naked shorting for which there is almost a total lack of transparency for individual investors.

When most investors look at their brokerage statement, they think that they own registered stock of the companies they have invested in. A registered holder is a shareholder who holds their shares directly with a company and have their names and addresses recorded in the company's share registry maintained by a transfer agent. Public investors don’t. They actually own a financial derivative of registered shares. Their brokerage firm is the nominee that holds the securities listed in their account in street name. Investors receive the financial benefits of registered stock ownership such as dividends and also can vote on all corporate affairs, but they don’t own the street name securities. Adding to the complexity, street name shares are a financial derivative of actual registered shares, all of which are owned by Cede, a subsidiary of DTCC.

Investors own a derivative security of a derivative security of the actual registered shares owned by Cede. This mind bending arrangement is at the heart of the current clearing and settlement system that covers virtually all stock trades in the US. The designers of the system largely were Wall Street firms who convinced government legislators and regulators that this is critical to the admittedly very effective system we now have. This was done to immobilize and dematerialize registered stocks in order to create a liquid market capable of trading billions of shares per day while virtually eliminating settlement risk. This objective was accomplished, but at the cost of making investors buy a financial derivative of a registered stock instead of actually owning the stock. A registered share is a distinct piece of property like a car or a house. This is not what investors own. They own fungible financial derivatives of registered stock or said another way, they own untraceable commodities.

In theory, for each registered share of a given company’s stock, Cede has issued a corresponding street name security. These are held by brokers who must be members of and hold accounts in DTCC in order to trade. These brokers and other participants trade street name securities among themselves. They have accounts at the DTC subsidiary of DTCC so that the DTC can track in real time of the number of street name securities held long and held short by every participating broker.

Brokers trading street name securities only rarely match a specific buyer with a specific seller. Instead they clear and settle through a very different process called continuous net settlement. Throughout the day individual brokers may execute hundreds or thousands of trades both long and short in a given stock. They do not settle each trade as it occurs, but rather they are buying and selling from an inventory. At the end of each trading day (actually on the settlement day of T+2), they sum up the number of shares bought and the number sold and add or subtract this to their account at DTC. They may have either a positive or negative number of total shares in street name.

Individual investors also have accounts at the DTC. Remember that investors do not own street name shares, but rather a financial derivative of street name shares. In theory, there are equal numbers of these financial securities and street name shares. When we buy or sell a share of stock, our broker executes the trade in street name securities. It is important to understand that the broker under net continuous settlement is almost never matching a buy order with a sell order, but is buying and selling from its inventory. They next credit or debit our account with a “second derivative to registered stock” security. This results in total lack of transparency to outsiders about who is buying or selling stock, but internally DTCC can track this in real time.

Who Actually Benefits from Stock Lending?

The biggest beneficiaries of stock lending are brokers. They lend stocks from their inventories of street name securities which are comprised of all of the stocks held in margin accounts of their customers. Individual investors almost never know that securities in their accounts are being lent and obviously don’t participate in the economic benefits. If you search hard enough, you can find a few ways to profit from lending stocks from your account, but the brokers do their best to discourage this. The bottom line is that brokers are making enormous profits without sharing them with customers who theoretically should be entitled to the bulk of the economics. Even worse, this goes against the economic interest of the broker’s customers. These securities are lent to investors who want to drive down prices and sometimes use short selling (and illegal naked short selling as I will shortly discuss) to manipulate stock prices down.

In addition to Wall Street brokers loaning out their customer’s shares, some of the large mutual funds like Fidelity and Vanguard and large pension funds knowingly lend their shares to short sellers. They are long term holders and see this as a way of increasing the return on their portfolios. Apparently, they feel that whatever bad motives the shorts may have, it won’t affect price appreciation of stocks in their portfolio. I can only scratch my head on that.

A Refresher on Illegal Naked Short Selling and Creating Counterfeit Shares

Reg SHO allows naked shorting of stocks by a market maker. This means that a market maker when given an order to short a stock can complete the trade without locating stock to borrow. Reg SHO allows the market maker two days until settlement (T+2) to locate stock to borrow. Actually, Reg SHO allows bona fide markers (whoever they are) to have six days (T+6) to locate shares to borrow.

If the market maker has not located shares to borrow by T+2, the National Securities Clearing Corporation (NSCC) subsidiary of DTCC steps in to guarantee settlement of the trade. They borrow shares from a broker who has a net positive balance of street name shares. The idea is to give the market maker time to locate shares and also to guarantee the settlement. If shares to borrow are not located, this is called a Failure to Deliver (FTD). If the market maker does indeed locate shares, they return them to the NSCC. In the event that the shares are not located, the broker from whom the NSCC borrowed shares can call for a buy-in which requires the market maker to buy the shares in the open market and return the cash they received. This in theory will alleviate the FTD. However, there are innumerable ways to get around the need to locate shares to borrow. Here are some:

Rolling over Positions is the Most Prevalent

- Market Maker “A” with the FTD can work in collaboration with Market Maker “B”. “A” locates and borrows shares from “B”. However, “B” uses a naked short to supply the borrowed stock.

- “A” no longer has an FTD.

- “B” is now naked short the shares and has six days to find a locate.

- If “B” does not find a locate, they have an FTD. “B” then can buy the shares from Market Maker “C” who executes a naked short, ad infinitum.

This is called rolling over a position and can be done for a very long time. Obviously, it requires a conspiracy between Market Maker “A”, Market Maker “B” etc.

No Buy-In

The broker who bought the shares for its customer that were naked shorted by Market Maker “A” may elect not to call for a buy without sounding any alarm bells. They have received shares from the NSCC and credited them into their customer’s account. An actual buy-in would be disruptive for both the broker and its customer so that it is an easy course of actions is just to ignore the FTD. The SEC lacks the resources and seems disinterested in forcing buy-ins.

Forget About It

The SEC lacks the resources and seems disinterested in actively policing FTDs. Market Maker “A” may be able to just ignore the FTD without penalty.

The Implications of FTDs

Here is what happens when an FTD is rolled over, no buy-in occurs or is simply ignored. Let’s use an example when Market Maker “A” receives an order to short 10,000 shares of XYZ at say $20.00, but can not immediately locate shares to borrow:

- A hedge fund delivers an order to short 10,000 share of XYZ to Market Maker “A”

- Market Maker “A” immediately shorts 10,000 shares without locating shares to borrow.

- Some customer(s) of Broker “X” buys the shares.

- The hedge fund receives $200,000 in cash from the customer(s) of Broker “X” at T+2.

- However, at T+2. Market Maker “A” has not located shares to borrow and deliver to the customers of Broker “X”.

- NSCC steps in to guarantee the settlement of the trade. It borrows 10,000 shares from a customer(s) of Broker “Y”.

- These 10,000 shares of XYZ are credited to the customer(s) of Broker “X”. They now show 10,000 shares of XYZ in their accounts.

- The problem is that the NSCC borrowed 10,000 shares of XYZ from customers of Broker “Y” and they are also credited with owning 10,000 share of XYZ.

- The customers of Brokers “X” and “Y” own the same 10,000 shares. This is how counterfeit shares are created.

- Because of continuous net settlement used by member firms of the DTCC, these shares are commingled in the inventory of the Brokers “X” and “Y” and can’t be traced to individual accounts.

- Customers of Broker “X” now own 10,000 counterfeit shares of XYZ, but they can’t be distinguished from legal street name shares.

- These 10,000 counterfeit shares can be loaned out to other short sellers.

- Market makers and hedge funds working in concert can create a virtually unlimited number of counterfeit shares.

Illegal Naked Shorting is a Winner’s Game

In my judgment, which is admittedly based on anecdotal evidence, certain hedge funds have been able to use illegal naked shorting to make short selling a winner’s game. Hedge funds acting through collaborating market makers can create huge numbers of counterfeit shares that can overwhelm buying demand. Illegal naked shorting also takes away a major disadvantage of short selling and that is the borrowing costs. If you are not actually borrowing shares, there may be no borrowing cost. Actually, brokers will usually charge hedge funds a borrowing cost even if the borrowed stock is counterfeit. It is just that the cost is much lower. This allows for (illegal) shorts to be maintained for a much longer period of time.

Tagged as borrowing cost for short sellers, failure to deliver stocjk, illegal naked shorting, lending stock to short sellers + Categorized as LinkedIn, Smith On Stocks Blog