Northwest Biotherapeutics: There could be Overwhelming Patient Demand for DCVax-L due to the Right to Try law (NWBO, $0.24, Buy)

Investment Thesis in Brief

I believe that it is now a matter of when rather than if DCVax-L is approved and becomes an integral part of standard of care (SOC) for newly diagnosed glioblastoma multiforme. I estimate that the worldwide addressable market is $5.5 billion and I would expect DCVax-L to penetrate a very significant percentage of the addressable market. Analysis of the blinded data from the ongoing phase 3 trial clearly demonstrates that patients are living longer than would be expected if they were receiving just SOC. Unless SOC is somehow delivering “never before seen” results the survival benefit can only be attributed to DCVax-L.

Management on the advice of its scientific advisory board has chosen not to unblind the trial in order to fully define the survival tail. They have not given guidance on how long this will take. However, I note that by August of 2018, the last patient enrolled in the trial will be three years out from surgery. I consider this the outer edge of when the trial will be unblinded. This is a sound scientific decision, but is frustrating to shareholders. Sadly, it has also allowed the wolfpack to continue to pound the stock with illegal naked shorting.

Will shareholders be forced to sit here watching wolfpack tactics reduce the stock price day after day? This is what has been happening in the last few days. However, a new dynamic has arisen in the form of the Right to Try law and this is the subject of this report. I think that later this year, investors will begin to anticipate meaningful revenues due to this law. I think that demand from GBM patients desperate for something that might improve their survival chances will be overwhelming and I calculate that for every 100 patients treated, the potential revenue stream could be $25 million and it seems likely that several 100s will seek treatment I think that as investors become firs aware and then convinced of the strong probability that this can occur, we could begin to see the stock reflect the value of the DCVax-L asset which is many multiples of the current wolfpack orchestrated stock price.

Structure of this Report

This report is organized into several sections;

- Key Points for those who want a quick overview of the report

- Key Investment Issues

- How the Right to Try Law Changes Access to Drugs

- Implications for Two Small Biopharma Companies: Northwest Biotherapeutics and Brainstorm Cell Therapeutics

- Quick Look at Brainstorm Cell Therapeutics

- Investment Implications for Northwest Biotherapeutics

- Comments from Brainstorm Cell Therapeutics Conference Call on Right to Try Law

Key Points:

- There are 11,000 patients newly diagnosed in the US each year with the deadly, life threatening brain cancer glioblastoma multiforme (GBM). So how many might be treated under the new Right to Try law? Approximately 50% of these patients die within 17 months or so from diagnosis and 70% die within two years when treated with standard of care (SOC). The law defines eligibility as a patient suffering from a life threatening disease who has no treatment options and cannot participate in a clinical trial. Does this mean that newly diagnosed GBM patients who have access to standard of care (SOC) might not be eligible? I don’t know.

- Approximately 50% of GBM patients treated with SOC progress within 7 months and they have a life expectancy of about 6 to 9 months. They are exactly what the law was designed for as there are no approved drugs for this indication that improve survival.

- I think that patients diagnosed with GBM and their families will scour the internet for new experimental treatment options. They will quickly come across DCVax-L and will move heaven and earth to gain access. I am comfortable in predicting that there are likely to be several hundreds, a thousand, or probably more requests from GBM patients in the US to access DCVax-L. However, not all will be eligible.

- Northwest can price DCVax-L as if it were an approved drug. Based on a comparison to the checkpoint inhibitors and CAR-T drugs, DCVax-L could be priced at $400,000 per course of treatment. However, I think that management will not push the price point to the highest that the market will bear. My best guess is that the price will be about $250,000 spread over 11 or more injections. If so, each 100 patients treated can give rise to a potential revenue stream of $25 million.

- The major gating factor for patients being able to access DCVax-L could well be that in order to manufacture DCVax-L, there must be sufficient tumor tissue available from a prior surgery.

- It is very likely that payors will go to great lengths to not reimburse DCVax-L (and other drugs) under Right to Try. Treatment may have to be paid for out of pocket, from grants or some other innovative source of funds. This presents an ethical quandary in that only the rich may have access to DCVax-L, However, there is also the quandary that this should not be a reason to prevent them from gaining access to a potentially lifesaving drug.

- One of the positive aspects of Right to Try is that it has much the same characteristics as a commercial launch so that when approval is ultimately gained, uptake in the broad population of GBM patients will be quick as sites will have treatment protocols in place and will have experience in seeking reimbursement.

- I believe that approval of DCVax-L is a matter of when rather than if. Management has said that it wants to make sure that the survival tail is fully defined so that timing of unblinding of the trial and regulatory approval is uncertain.

- The wolfpack is in full attack mode on the stock as has been the case for several years. Illegal naked shorting is going on in a massive way according to my sources. In the face of the release of some extremely positive clinical data and passage of the Right to Try law the wolfpack has successfully blocked any positive stock reaction and are now walking the stock down day by day. This type of stock manipulation is one of the largest criminal schemes in the US.

Key Investment Issues

DCVax-L Clinical Data is Extremely Promising

I have great confidence that the data on DCVax-L will lead to its approval. This is based what that we have seen from blinded results of the phase 3 trial, phase 1/2 data, findings in the information arm of the phase 3 trial and compassionate use experience. I am not alone as the two lead investigators on the phase 3 trial, Dr. Keyoumers Ashkan in Europe and Dr. Linda Liau in the US, have both stated that DCVax-L is a potential breakthrough in the treatment of glioblastoma multiforme. Additionally, 69 physicians and scientists involved in the phase 3 trial just co-authored a manuscript that concluded that patients in the trial are living significantly longer than would be expected with standard of care (SOC). Unless SOC in the trial is delivering “never before seen” positive results which is extremely unlikely, this improved survival can only be attributed to the therapeutic benefit of DCVax-L.

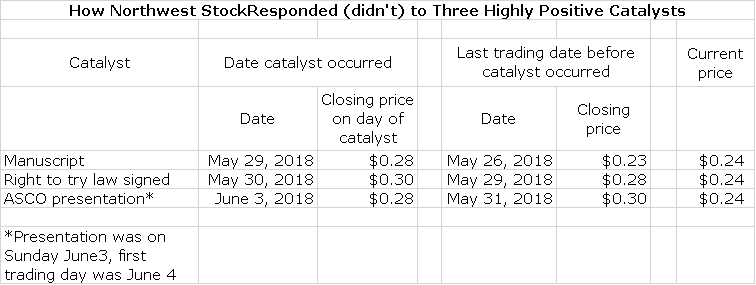

Wolfpack is Aggressively Stepping up Shorting Attack

There have been three extremely positive pieces of news on DCVax-L since May 29: the release of the manuscript, emotionally wrenching patient testimonials from patients at ASCO about DCVax-L efficacy in very late stage GBM and passage of the Right to Try law. Each of these should have led to a meaningful increase in the stock price. In a shocking and brazen display of their ability to manipulate stock prices, the stock price has been held flat and they are walking the price lower on a daily basis.

Despite this, the wolfpack continues the attack challenging these results in blogs, flooding message boards with spurious arguments and heavily pressuring the stock with naked shorting. With the cooperation of market makers, the wolfpack can overwhelm buy orders by selling literally millions of shares of counterfeit stock. They have been walking the stock down a penny or so each day.

While the bloggers who work in concert with the wolfpack have launched a coordinated negative campaign, in actuality the wolfpack doesn’t really need their attacks to drive the stocks down. This just provides cover. Why the wolfpack continues to attack and try to severely damage a company that key opinion leaders believe may have a breakthrough for an aggressive cancer is deeply disturbing. They are so driven by greed for money that this transcends all; they have lost their souls.

Northwest Doesn’t Want to Unblind the Phase 3 until the Extent of the Survival Tail is Determined

Assuming that the shared enthusiasm of the two lead investigators on the trial, 69 co-authors of the manuscript and “little” me is correct, the probability of DCVax-L approval is a matter of when and not if. Still, CEO Linda Powers has said that the trial will continue until the clear outline of the survival tail can be defined. What is a survival tail? This is a relatively new term that came into use with the advent of immunotherapy drugs. Before then, cancer trials used median progression free survival and median survival as key endpoints for trials. The checkpoint inhibitors- principally Yervoy, Opdivo and Keytruda- changed the way we think of determining efficacy for immunotherapy cancer drugs.

These drugs had the unique characteristic in that a small, but meaningful number of patients experience very long survival that in some cases approaches a cure. Let me try to put this survival tail in perspective by looking at results for the checkpoint inhibitor Opdivo in the CHECKMATE-017 and CHECKMATE-057 trials in non-small cell lung cancer which indicated that out of every 100 patients treated, 9 or 10 more of the Opdivo patients would be alive at three years than if they had received standard of care.

- CM-017 enrolled patients with second line squamous NSCLC: 16% of Opdivo patients were alive at three years (21/135) versus 6% on docetaxel (8/137) (HR 0.62). Put another way, out of every 100 patients treated, 10 more Opdivo patients would be expected to be alive at three years than if they were treated with docetaxel.

- CM-057 enrolled patients with second line non-squamous NSCLC: 18% of Opdivo patients were alive at three years (49/292) versus 9% of docetaxel patients (26/290) (HR 0.73). Out of every 100 patients treated, 9 more Opdivo patients would be expected to be alive at three years than if they were treated with docetaxel.

So what about the survival tail for DCVax-L? Historical data indicates that about 15% of glioblastoma patients treated with standard of care are alive at three years. In the manuscript just published on the blinded data from the phase 3 trial, 182 patients were alive at three years post-surgery. Of these, 44 patients (24%) have lived longer than three years. If this data in 182 patients were indicative of the results for all 331 patients, 24 out of every 100 patients given DCVax-L would be alive at three years as compared to the 15 expected based on historical results. This improvement of 9 patients out of every 100 living longer would be comparable to Opdivo in second line lung cancer. Because this data includes the outcome of SOC patients, the survival tail for DCVax-L treated patients would almost certainly be better.

Investors are pressing management to unblind the trial. However, the scientific advisory board acting on the opinion of independent statisticians have advised Northwest to not unblind in order to more fully define the survival tail. It is possible that we could see an update of the data analyzed in the manuscript in coming months. Because the data cutoff for the manuscript was March 2017, the data now has matured by more than a year. By August of 2018, every single patient in the trial will be 36 months post-surgery. Perhaps, this possibly could be the very latest date for unblinding the trial, but I can’t say for sure.

Right to Try Law Could Change the Investment Equation

The wolfpack attack is banking on the uncertainty of when topline data will be released. The goal is to drive the stock price down and force one or more small financings at sharply discounted prices from the current level as NWBO is financially distressed. The primary goal before the publishing of the manuscript to drive NWBO into bankruptcy seems highly improbable. Once the topline data is released and assuming that it is positive as expected, the investment equation changes in a manner that not even the wolfpack can control as big pharma would almost certainly enter into licensing or co-promotion agreements or just outright acquire the Company.

Before the unblinding of the phase 3 trial, the Right to Try law could change the wolfpack calculation. As discussed in-depth in this report, this could result in the beginning of a meaningful revenue stream later this year. Importantly, this could also be very important for the ultimate commercial launch. The major centers who participated in the trial will likely be involved in treating Right to Try patients. They will establish protocols and will work on gaining reimbursement from payors. Hence, at the time of the launch, the uptake into the broad GBM patient population could be rapid.

How the Right to Try Law Changes Access to Drugs

The Right to Try law was signed into law by President Trump on May 30, 2018. This has the potential to create a new dynamic in drug development. Under current laws, before patients can have “easy” access to a drug, it must go through rigorous clinical trials to establish that the drug has acceptable efficacy and safety when balanced against the severity of the disease it is intended to treat. The process of drug development can be lengthy. I have not done a detailed analysis, but I estimate that the fastest time from the point when a drug first goes into humans until it is submitted to regulatory authorities is around four years or so and more often six or more years. The regulatory review then takes more time. In the US, the regulatory review period is supposed to be nine months or less. However, in many cases, if the FDA can’t complete the review on time they can issue a Complete Response Letter (CRL) that can extend the review by another six to nine months or more.

The FDA has an incredibly difficult job to do and while they make mistakes, I think that they make an invaluable contribution to society in scrutinizing safety and efficacy before drugs are made widely available. However, the slow and deliberate pace of clinical development and regulatory review is justifiably criticized.by patients (and their advocates) who suffer from life threatening disease. For people who have exhausted all therapeutic options for treating their disease as in the examples of aggressive cancers like glioblastoma multiforme (GBM) or ALS, it is beyond frustrating that they can’t have access to experimental drugs that offer their only hope (even if quite slim) for extending their lives. The Right to Try law is intended to give such patients the one remaining chance they have, i.e. access to an unapproved experimental drug.

Critics argue that this can already be done through existing compassionate use programs, but I can assure you from personal experience that this is not the case. The only son of dear friends just died from an aggressive cancer. WE knew he was dying and we tried to get access to an experimental drug through compassionate use. Along with the Company and the physician who would treat him, we jumped through one bureaucratic hoop after another requiring substantial time commitments for all. Finally, after several months, we got everything approved. He moved to the top of the list for treatment just as he died. I don’t know if the drug would have worked as it was an aggressive sarcoma, but boy I wish we could have given it a shot. It is patients such as these that the Right to Try law addresses.

Implications for Two Small Biopharma Companies: Northwest Biotherapeutics and Brainstorm Cell Therapeutics

Right to Try has important implications for some small biotechnology companies working on drugs for life threatening disease who usually have limited financial resources. Big biopharma companies are much more risk adverse so that for many (not all) it is usually the case that really cutting edge technologies and drugs are first tackled by small entrepreneurial companies. Big pharma usually sit back and wait until a drug is reasonably well understood and then license the drug or acquire outright the Company developing it. The current regulatory process favors big risk adverse biopharma companies as it puts financial strains on small companies who then must turn to the big guys to complete development and commercialization.

This dynamic could be meaningfully changed by Right to Try because it may allow small companies in some very limited cases to develop meaningful revenues streams prior to approval and make it easier for them to access capital more easily. In this report, I discuss how this might work for Northwest Biotherapeutics and Brainstorm Cell Therapeutics which is in a phase 3 trial with NurOwn for ALS. I am optimistic about DCVax-L while I am quite skeptical about NurOwn.

Quick Look at Brainstorm Cell Therapeutics

In my opinion, the mechanism of action of NurOwn is not well defined and the clinical trial evidence is inconclusive. The phase 2b trial that was the basis for starting the phase 3 leaves me with a lot of questions. It was a small 36 patient trial that was randomized 24 patients on NurOwn and 12 on placebo. The primary endpoint was change in ALSFRS-r at 24 weeks and BCLI announced that NurOwn showed statistical superiority at 24 weeks. The study also looked at biomarkers.

I am skeptical on this trial for several reasons. It was very small. Also, in my conversations with Cytokinetics and Neuralstem who are also developing drugs for ALS, based on their experience I conclude that ALS sometimes progresses sporadically in a stop and go process. Both CYTK and CUR felt that trials using ALSFRS-r as an endpoint should go at least 52 weeks. I am also surprised that BCLI has not followed the 48 patients in the trial to determine if there was a durable effect. This is really eye brow raising.

BLCI is now in a phase 3 trial involving 200 patients that will be randomized 1:1. They have enrolled 70 of the 200 patients and will report topline results in 2020. NurOwn is injected into the fluid-filled space between the thin layers of tissue that cover the brain and spinal cord. There are three injections at two month intervals,

I wish NurOwn well and hope that my skepticism is misplaced and that the drug is effective in ALS, but I can’t consider it as an investment based on what I know. To me there is scant evidence to believe that NurOwn will be effective, but it does seem to be safe. Despite my considerable skepticism, if I had ALS, I probably would take the drug if given the option. It provides hope in a hopeless situation and that alone is a therapeutic benefit.

Investment Implications for Northwest Biotherapeutics

I am much more positive that Northwest Biotherapeutics’ DCVax-L is an effective drug and indeed could be a breakthrough for GBM. It is nearing completion of a 331 patient phase 3 trial that has been running for over a decade. Investigators in the trial have stated that patients seem to be living longer than expected in this trial. A recent analysis of blinded data suggests very strongly that DCVax-L is meaningfully extending the lives of patients over and above standard of care (SOC). The lead US and European investigators in the trial have both said that DCVax-L is a potential breakthrough for the treatment of newly diagnosed glioblastoma multiforme.

In addition, the phase 1/2 trials involving 20 patients indicated that median overall survival for DCVax-L was over twice that of standard of care. Results from 31 patients in the information arm of the phase 3 trial were also encouraging. Finally in a recent presentation at ASCO five patient testimonials showed that in these cases that patients who were told they had weeks to live received DCVax-L are cancer free and have lived for years. Importantly, the side effects with DCVax-L are trivial.

I think that DCVax-L is a perfect drug for the Right to Try law. If I had any stage of glioblastoma multiforme I would move heaven and earth to get access to the drug. There is considerable evidence suggesting strong efficacy. Serious side effects are extremely rare so that it doesn’t impact the quality of whatever life is remaining. It is easy to administer as it is given with a series if intradermal injections.

Comments from Brainstorm Cell Therapeutics Conference Call on Right to Try Law

To date, Northwest has provided no significant statements on how they view the Right to Try law’s effect on DCVax-L. In contrast, Brainstorm has communicated at length and held a conference call on June 7, 2018 for investors and patients that lasted for one and one half hours. I listened to the call to hear issues that Brainstorm chose to emphasize that could be applicable to Northwest.

BCLI management emphasized the important difference between Right to Try and compassionate use programs:

- Companies don’t have to alert the FDA on serious adverse events as they occur. They can update the FDA once a year.

- Pricing under compassionate use programs is based on a markup over cost of manufacturing. This required hiring an independent accounting firm to determine and validate cost of manufacturing. BCLI can set the price on NurOwn without this requirement.

- To treat patients, they don’t have to go through an Internal Review Board in order to treat patients. This decision is left to the patients and physicians can make the decision.

In this section, I go over the key points that were made in the call and their implications for Northwest

1. Patients participating on the Call were so desperate

ALS patients and caregivers were part of the call. It was heart breaking to see how desperate they were for even a tiny glimmer of hope. Most said they would go anywhere and do anything to get access to NurOwn and would mortgage their homes to pay for it. Some seemed to believe that there was strong evidence that NurOwn could not only slow the progress of ALS, but potentially reverse it. As I previously discussed there is only the faintest evidence of any therapeutic effect and I would give odds that the phase 3 trial fails. Nevertheless, I think that there will be enormous demand from ALS patients and if I had ALS I would likely take the drug if offered.

Implications for Northwest

Glioblastoma is no less desperate of a disease than ALS. Results with standard of care indicate that 50% of patients will die in 17 months or so and 70% will die by year two. I think that GBM patients will be as desperate to get access to DCVax-L.

2. Which Patients will be Selected and How?

BCLI Management was not specific on the criteria that would be used to select which patients to treat. The definition in the Right to Try law is a patient with a life threatening disease who has exhausted all options and can’t participate in a clinical trial. This encompasses most of the 20,000 patients with ALS in the US. BCLI said that they would largely let key opinion leaders be the primary determinant of defining who is eligible.

Implications for Northwest

A strict reading of the Right to Try law could suggest that newly diagnosed GBM patients would not be eligible as they would have access to SOC. On the other hand, 50% of patients die in 17 months or so and 70% in two years. Who among us would not jump at the chance to potentially improve their odds of survival by adding DCVax-L to SOC? This is particularly the case because there are almost no troublesome side effects that interfere with quality of life. There is going to be enormous pressure from newly diagnosed patients to receive DCVax-L.

Approximately 50% of patients treated with SOC progress within 7 months. When this occurs, patients have a life expectancy of about 6 to 9 months. All of these patients would be eligible; they are exactly what the law was designed for as there are no approved drugs for this indication that improve survival. The only gating factor is whether there is sufficient tumor mass preserved from a prior surgery to manufacture the vaccine.

Until recently, I was uncertain that DCVax-L might warrant usage in relapsed patients as my impression was that immunotherapies require months to be effective. In that case, DCVax-L might only be effective for newly diagnosed patients. However, at the recent ASCO meeting Northwest presented testimonials from two patients treated under compassionate use that changed my mind. A 60 year old man and a young mother had each been surgically resected not once, but three times. Both were told they had just weeks or months to live. After receiving DCVax-L, they are alive three and four years past the point when doctors said they would die.

3. Who Will Treat the ALS Patients and where will they be Treated?

NurOwn requires some experience and knowledge to administer. Not all neurologists will be familiar with the steps that are required to administer the treatment. It is almost certain that only physicians participating in the phase 3 trial now underway at six centers will treat patients. With only six centers, there will be an issue with how many patients can be treated as they are also treating patients in the phase 3 trial. Patients have to come back three separate times to receive an administration so that this might introduce some kind of geographic factor into patient selection although I think that most ALS patients would do anything and travel any distance to get NurOwn.

The limited capacity to treat means that there will be exclusion criteria. Obviously, those most likely to benefit will be at the head of the line, but making such determinations will be painful. BCLI said that it will rely heavily on physicians to make this call. They said that they hope to issue a policy statement on this in a relatively short time. Mention was made of using a lottery. In the near term, patients wanting to participate can go to the BCLI website in order to be put on list for possible inclusion in Right to Try.

Implications for Northwest

The phase 3 trial for DCVax-L took place at 41 centers worldwide (most in the US) and as many as 69 physicians took part in the trials. This provides much better geographic reach and physician capacity than is the case with NurOwn. DCVax-L is easy to administer as it is given as an intradermal injection and there are almost no dangerous side effects that may accompany administration. The overall procedure is much quicker that is the case with NurOwn so a single oncologist could treat many more patients each day.

4. What Kind of Manufacturing Capacity Does BCLI Have?

Brainstorm said that they currently have manufacturing capacity to treat 100 patients under Right to Try in addition to the 200 being treated in the phase 3 trial. They did not put this in perspective as to what period of time this covered. Nor did they talk about the ability to expand manufacturing and if they did decide to do so, how long it would take. They have just filed a $100 million shelf registration and I think it is a fair guess that they may raise capital under the premise that it would be used to expand manufacturing capacity to meet demand.

Implications for Northwest

The manufacturing for DCVax-L has been proven through support of the phase 3 trial and there is capacity in both the US and the UK. All of the manufacturing requirements for phase 3 have been completed as DCVax-L is prepared for each patient shortly after surgery and all of product needed for the series of 11 or more injections is cryopreserved. All manufacturing capacity can be devoted to Right to Try patients. As an outright guess, I think that they can produce product for several hundred, a thousand or perhaps more in a year. NWBO has not commented on this estimate.

5. What is the Cost of Manufacturing?

BCLI management did not give any indication as to the cost of manufacturing. They did say that this is an autologous product whose manufacturing starts with getting bone marrow from the patient and processing it into NurOwn. It is very labor intensive and hence costly. They referred to the manufacturing process used to produce CAR-T cells as a comparable manufacturing process. I think that the per patient manufacturing cost for CAR-T cells is in the $35,000 to $40,000 range.

Implications for Northwest

NWBO has not given guidance on the per patient manufacturing cost of DCVax-L. My guess is that it is on the order of $40,000.

6. How will NurOwn be Priced?

BCLI management did not make any comments on pricing, but I think it would almost certainly be well into six figures. This is common for drugs that treat life threatening diseases affecting a small patient population.

Implications for Northwest

I have asked NWBO about pricing and they quite predictably haven’t given any details but they did made an interesting comment. They said that they thought that the $325,000 price tag for just a single injection of the new CAR-T drug Yescarta is excessive, especially given that it may at best be medically important in 30% or less of patients. I take this as meaning that they might price at a lower level even though the market could probably bear $325,000.I have also asked about how many patients they think might want to use DCVax-L under Right to Try. Again, no comment.

From this scanty amount of information, I have come up with an idea for pricing. Management has neither endorsed nor refuted my assumptions. Actually, they haven’t yet heard them. Remember that DCVax-L in the phase 3 clinical trial was given as intradermal injections at days 0, 10, 20, and at weeks 8, 16, 32, 48, 72, 96 and 120. Here is my suggestion. How about pricing the first three or so injections at about $40,000 which is maybe $5,000 over the cost of manufacturing. Then each of the subsequent seven injections would be priced at $30,000. If at some point, the treatment is judged to be ineffective, it could be halted and no further costs incurred. In terms of economics for NWBO the Yescarta model of “all up front” would be the best. However, for the patient and payor, I think that there would be great enthusiasm for my model.

7. Paying for NurOwn

BCLI management c stated that if insurance companies refuse to pay for therapy provided under Right to Try (very likely in my opinion), this would mean that only the rich who can pay out of pocket would have access. They believe this is unacceptable to society. However, they raised the interesting philosophical point that if it is the case that only the rich can pay, should we deny them access because not all have access. Management alluded to finding third party funds for at least some of the poor. I would think that there might be money available from foundations like the Bill and Melinda Gates Foundation. BSCI says that they are actively pursuing a solution that would pay for some of the poor.

Tagged as DCVax-L and Right to Try law, Northwest Biotherapeutics Inc. + Categorized as Company Reports, LinkedIn

Larry, did the SAB just make this decision off of the spring refresh 2018 data, or are you referring to their prior decision from last year?

I am referring to what Linda said at ASCO. She did not give a time perspective. The SAB comment was likely based on the March 2017 data as reported in the manuscript.

Larry,

Given the rxcellent results, and with the platform being needed, valuable in more ways than one, and seemingly derisked, what’s to keep a larger pharma from trying to scoop up NWBO?

I’m a little skeptical about Right to Try. I don’t think insurers would pay for DCVax-L even if it was priced at $1 because they wouldn’t want to set the precedent of paying for Right to Try drugs.

Given that, I don’t think your pricing suggestion would be effective. I also think the traditional pricing model won’t work. While $250k is probably a reasonable retail price, after going through an arduous process of evaluating each patients’ ability to pay they’ll likely steeply discount the price for the majority of people who can’t afford $250k. In the end, after the agonizing process, they’ll wind up realizing closer to what they’d be getting under compassionate use.

I don’t envy NWBO or any company in this circumstance. Maybe their best bet is to not take advantage of the law and instead hope that the FDA will act expeditiously when they do unblind to start the process of getting the payors to cover the cost.

A question: How similar was the 2014 Hospital Exemption Program in Germany to right to try? My impression was that the regulatory body “blessed” DCVax-L but the public funding bodies refused to pay for the drug. It would seem that there would have been an opportunity for wealthy people to be able to pay out of pocket for the drug, much like we now appear to have in the US with Right to Try and no institutional payor requirements. However, the company has never reported having treated paying patients in Germany.

I guess this makes me look like a basher. However, I would say this is on NWBO management. I believe the company should have provided regular updates on their progress regarding Hospital Exemption.

Here are my thoughts for the next few months. I believe the second interim review the company reported is underway will be based on March 2018 data (1 year after the review published in the academic journal). I also think that the company will make a decision on unblinding after seeing the data from this second review.

One encouraging note is that in her ASCO presentation, Linda Powers said she hopes to have business-related news to report in the coming “weeks” if my memory serves. I believe big pharma companies and reputable financial investors all said something to the effect that they would only consider investing after NWBO published peer-reviewed data. Ms. Powers is now following up on those statements to see if they will now step up to the plate.

Smith, what is your take on the recent NWBO P3 trial discussed by LL at the SCO conference?