Northwest Biotherapeutics: (NWBO, Buy, $0.35) Management Issues Guidance That DCVax-L Phase 3 Trial Results Will Be Released Sometime After Labor Day

Investment Overview: Highly Asymmetric Outlook

Northwest Biotherapeutics has guided that it will report results of the phase 3 trial of DCVax-L in newly diagnosed glioblastoma (GBM) sometime after Labor Day. This results in a highly asymmetric outlook for the stock price. In this report, I present a plausible hypothesis that over the next year the stock could trade to $5 to $8 if investors conclude that the trial is a success and that FDA will approve DCVax-L as an addition to standard of care. If the trial fails, I think that the stock could plunge to a penny or two or quite likely NWBO could go bankrupt. So, the upside could be $5+ against a downside of $0.35. The current market capitalization is $228 million based on shares outstanding and $400 million if every outstanding warrant and option is exercised. The stock price of $0.35 obviously suggests extreme skepticism that there is a reasonable chance for success in the trial, but data released on mortality from the still blinded trial encourages me that DCVax-L is meaningfully extending survival. See my report of January 2020, “Why I Believe There is a High Probability for Approval of DCVax-L” .

Despite reasons for optimism, the trial could fail or produce disappointing or equivocal results; trial outcomes are notoriously unpredictable. However, this is always the case so that investors essentially are weighing the odds of trial success against failure for all emerging biotechnology companies. I think that the upside for NWBO in the event of success could be a market capitalization of $ 6 to $9 billion which might translate into a stock price of $5 to $8. How do I get to the latter numbers? My approach is to compare the valuations of 11 emerging biotechnology companies focused on T-cell engineering (CAR-T and TCR). These are reasonable comparables to Northwest Biotherapeutics, although not exact. (I go into detail later in this report on why I view these as good comparables). Right now, most investors are unaware of NWBO or are extremely skeptical of DCVax-L. With success in the phase 3 trial, investors’ attitudes could turn to enthusiasm as is the case with the T-cell engineering companies. If so, we can look to the valuations of these companies as a guide to the potential valuation that investors might place on NWBO.

NWBO has struggled mightily to get to the point of having a data readout on DCVax-L that if successful, would be a medical breakthrough and a commercial home run. To repeat myself, there is a reasonable chance for success. Later in this report, where I compare the fundamental outlook for NWBO against the T-cell companies, I conjecture that if NWBO was only now coming public, that it might garner a market capitalization of $2 billion or more. This report discusses the reasons for this disparity from its current market capitalization.

There is more than a reasonable potential for investor skepticism and disinterest to flip 180 degrees to enthusiasm. This all hinges on the results from the phase 3 trial of DCVax-L in GBM. If the results lead investors to believe that DCVax-L will gain approval as part of standard of care for newly diagnosed glioblastoma, the upward move in the stock could be stunning. In the previous paragraph, I suggested that the current fundamentals of NWBO could justify a $6 to $9 billion valuation if the trial results are clearly successful. However, this price increase probably would not occur over night.

- There is almost no research coverage of NWBO so that institutional investors are largely unaware of its fundamental situation. It would take time for analysts and institutional investors to come to understand DCVax-L.

- The data release will almost certainly have some points of confusion or disappointment even if the overall outcome is quite positive.

- It is often (almost always) the case that when results of a trial are released that it takes time for the medical community to study and come to understand the results. They almost always start from a position of skepticism.

- NWBO has been and continues to be the subject of a powerful stock manipulation scheme and it is very likely that investment banks and hedge funds involved in this scheme who are heavily short the stock (largely through illegal naked shorting) could attack the results.

- Finally, NWBO’s cash reserves are running on empty and the Company would immediately need to finance.

These factors suggest that initially there will not be a dramatic jump in stock price. Just as a wild guess based on nothing but intuition, I think the stock might increase to $1.00 with a clearly positive trial outcome and at that point the Company would raise money putting a temporary damper on the stock. With the financing behind it, I think we could then see the stock move toward my price target of $5 to $8 over time.

Release of Phase 3 Results is Imminent; What We Might See

We will soon know the results of the phase 3 trial. In a July 24 press release, Northwest Biotherapeutics guided that “In light of significant progress…., the Company currently anticipates that Trial results (the Phase 3 trial of DCVax-L) will be ready for reporting sometime after Labor Day in the month of September. The Company will be consulting with its Principal Investigator and experts on the appropriate venue and manner of presenting the Trial results.”

Ordinarily, companies just state statistical results for the primary and perhaps some secondary endpoints along with safety information. I think that this data release will be more extensive and more informative. I think that NWBO may disclose significant additional data such as sub-group analyses and particularly data on the all-important durability of response (survival tail). Blinded data from the phase 3 trial is strongly suggestive that there is a medically important survival tail in the trial. If so, this should be readily discernible as there will be over four years of data for the last patient enrolled in the trial and longer for all others. As a reference point, with current standard of care (SOC), historical trial results show that 50% of SOC patients are alive at 17 months after treatment, 30% at two years, 15% at three years, 8% at four years and 5% at five years. Any meaningful survival benefit for DCVax-L should be readily apparent.

So, at long last we will see the data from this important trial. If the results are positive, DCVax-L could become part of standard of care for newly diagnosed glioblastoma. Also, the technology of dendritic cell vaccines would be validated, indicating that it could be effective in treating other (most) solid tumors. This would be a major breakthrough from a medical perspective and a homerun from a commercial standpoint.

Price Target Thinking

If the DCVax-L trial fails, Northwest is likely to plunge to a penny or two or even go bankrupt. So, we know the downside is about $0.35. In this report, I present a case based on comparison to peer companies that the market capitalization could over time increase to $6 to $9 billion and possibly more if the trial is successful. To translate that into a future stock price, we must determine the number of future shares. The current number of outstanding shares is about 650 million and there are another 480 million potentially dilutive shares stemming from options and warrants so that if every potentially dilutive share is converted, there would be about 1.1 billion fully diluted shares outstanding. Incidentally, the exercise of the options and warrants might bring in $100 million over time. The current market capitalization based on 650 million shares is $228 million and is 400 million based on 1.1 billion shares.

NWBO is desperately in need of cash so that if the DCVax-L trial is successful, investors should expect a financing to quickly follow. Awareness of this could be an overhang that could slow the initial surge in price that would be expected with positive results. For the sake of illustration, let’s assume that the stock rises to $1.00 (slightly over $1 billion of market capitalization) and the Company raises $100 million by selling 100 million shares at $1.00. This would increase the fully diluted share count to 1.2 billion. With the financing behind it, the stock might then begin a rise to a valuation of $6 to $9 billion comparable to peer companies. This would lead to a share price of $5 to $8. This is clearly an asymmetric investment opportunity in which the upside for a clear trial success could be $5+ and the worst case downside based on bankruptcy is $0.35.

I would be amazed if this hypothesis on price behavior is anywhere near accurate, but I think it gives investors a starting point in thinking about an investment in NWBO. There are all number of other factors that could come into play. There could be substantial excitement that coupled with short covering could cause a dramatic overshoot for the stock on the upside as the investment community transforms from almost total skepticism to wild enthusiasm. There is also the possibility that the Company could raise substantial capital through a corporate collaboration negating or lessening the need for an immediate capital raise. NWBO might also be acquired outright.

On the negative side, there could be an attempt by the wolfpack to try to initially blunt an upside move as they rush to cover shorts, both legal and illegal. The wolfpack is a name that I have coined for a cabal of investment banks and hedge funds that manipulate stocks through heavy reliance on illegal naked shorting. Northwest has been an in the crosshairs of the wolfpack for over five years. For more detail on how this stock manipulation scheme is executed and who is involved refer to my recent ten blog series on illegal naked shorting. See this link. https://smithonstocks.com/?s=illegal+naked+shorting

Why Is Northwest Selling at $0.35 Per Share If There Is Meaningful Potential for Success in the Phase 3 Trial?

One can never predict with total confidence the outcome of any clinical trial. However, the blinded data that has been released on the phase 3 trial has been highly encouraging. See my report Why I Believe there is a High Probability for Approval of DCVax-L https://smithonstocks.com/northwest-biotherapeutics-why-i-believe-there-is-a-high-probability-for-approval-of-dcvax-l-nwbo-buy-0-21/?co=northwest-biotherapeutics This data suggests that there is more than a reasonable chance that the trial will be a success. Based on my evaluation of peer oncology companies, a market capitalization of anywhere from $1 to $4 billion would be conceivable, in my opinion. So why the disconnect in which the market capitalization of NWBO is $228 million based on 650 million shares outstanding and $400 million if every outstanding warrant and option is exercised.

In my lengthy career, I can think of few if any situations which rival the skepticism currently heaped on NWBO. However, this could change dramatically. The following sections discuss reasons why I believe that NWBO could turn from an ugly duckling into a beautiful swan. The following sections discuss some of the issues that have impacted the stock price.

Dendritic Cell Vaccine Treatment Was Initially Viewed with Skepticism

DCVax-L is an immunotherapy that unfortunately was ahead of its time. The concept of the technology is to use a patient’s own cells to treat their cancer. Monocyte progenitor cells are obtained through a blood draw and then through cell culturing outside the body are differentiated into dendritic cell precursors. These are exposed to a lysate made from cancer tissue removed during surgery from the patient which contains antigens of the tumor. The dendritic cell precursor takes up these antigens. They are then reinfused into the patient where they mature into dendritic cells that present these antigens to helper T-cells which triggers an adaptive immune response to the cancer. This process is called autologous cell therapy.

When the trial began over twelve years ago, big pharma was focused on traditional small molecule research and was oblivious or skeptical of immunotherapy and could not scarcely conceive of using living cells as medical therapies. On a scale of one to ten, skepticism registered at a ten. So, at the outset, there was virtually no interest in or awareness of DCVax-L from either the industry, medical or investment community. This made raising capital difficult and expensive. Back then the first meaningful immunotherapy technology, monoclonal antibodies, was just a faint blip the radar screens of big pharma. They were all about small molecules.

DCVax-L was also viewed as a therapeutic cancer vaccine which was a kiss of death as numerous other attempts to develop a cancer vaccine (using different technologies) had failed. In short, almost all of the major biopharma companies were oblivious to or gave DCVax-L no chance for success. Wall Street investors and analysts were equally dubious about providing capital to Northwest. So, almost the entirety of the biopharma research and investment world felt at the outset, that there was no chance for the trial to be successful.

DCVax-L is a Logical Extension of Immunotherapy Drug Development

Things have certainly changed in the last 13 years as immunotherapy, led by monoclonal antibodies, is now the driving force in biopharma research. In particular the checkpoint inhibitors-Yervoy, Opdivo, Keytruda, et al- have had a dramatic impact on cancer treatment since they were introduced in the 2011 to 2015 period. More recently, autologous T-cell therapy (CAR-T and TCR drugs) have captured the interest and imagination of big pharma and immunotherapy has become the tip of the spear for biopharma drug development of oncology drugs and investors are showering the biotech industry with cash to conduct clinical trials. Big pharma attitudes and investor interest are 180 degrees different from when the DCVax-L trial started in 2007.

In today’s world, dendritic cell technology looks much more interesting. It is logical given the success of monoclonal antibodies produced by B-cells and T-cells engineered to attack cancers to look to other key cells of the immune system for drug development. Indeed, there is great focus on natural killer cells ( I plan to write on this soon). So, it is logical to focus on the dendritic cell which plays a central role in instigating an immune response from B-cells and T-cells to attack cancer. Perhaps, DCVax-L’s time has come.

DCVax-L Technology Uniquely Addresses Neoantigens

Another big concept in current cancer therapy is targeting neoantigens. Monoclonal antibodies, targeted cancer therapies and CAR-T drugs target a specific antigen (molecule) on a cancer cell. However, cancers mutate over time so that the expression of an antigen that is the target of these drugs may lessen or even disappear over time. Moreover, within a given cancer there may be different mutations that express distinct antigens. Hence, the pre-selection of an antigen that characterizes monoclonal antibodies, targeted therapies and engineered T-cells could result in the drug not being effective if the cancer does not express or under expresses that antigen. Hence there is a great deal of research to determine just what antigens are being expressed in the tumor. This is called determining neoantigens.

Dendritic Cell Cancer Vaccines Make Sense in Today’s World

Wouldn’t it be great to engineer dendritic cells to express neoantigens? Yes, it would and that is exactly what NWBO has done with DCVax-L. Its technology is based on taking monocytes from the blood of a cancer patient. These are progenitor cells that through multiple differentiations become dendritic cells. These monocytes are cultured to produce a precursor to the ultimate dendritic cell in a process that has been developed by NWBO. The other important step in the technology is to take cancer tissue removed from the surgery of glioblastoma patients and lyse it. The resulting lysate carries the neoantigens of the patient. The dendritic cell precursor is then exposed to the lysate. When it is reintroduced to the patient, it displays the neoantigens through the MHC complex to helper T-cells which orchestrate the attack of the adaptive immune system on the cancer.

Hence, the biological hypothesis behind DCVax-L is logical and indeed elegant. However, it has been my experience that the biology of the human body is so complex that real life experience can differ substantially from a hypothesis. Hence, only clinical data can substantiate the hypothesis.

Why Aren’t Other Companies Developing Dendritic Cell Products?

You are no doubt asking the question that if DCVax-L is so promising, why aren’t other companies following its technology lead. In regard to big pharma, my response is that they have been followers for every major biotechnology innovation-recombinant DNA, monoclonal antibodies, anti-sense, RNA interference, gene therapy, et al. They usually await technology validation before entering a technology and most often enter through acquisition or collaboration. So, the lack of presence of big pharma is par for the course.

But what about small, innovative biotechnology companies. Where are they? This is harder to answer, but let me give it a try. There is a tight link between venture capitalists, investment banks and emerging biotechnology companies. They have an intermingling of interests and work in close coordination; you might call it a cabal. The venture capitalists need the investment banks to take their companies public and then support them in the aftermarket. Venture capitalists need the investment banks to provide liquidity and an exit strategy and the investment banks are paid richly to do this. There is mutual back scratching. So, a company that is fortunate enough to be in this club is provided capital and heavy promotion through investment bank research. Northwest has never been part of this crowd.

There was also a stigma with its technology. As I mentioned earlier, DCVax-L was a cancer vaccine and in the late 1990s and early 2000s there were innumerable failures such as Cell Genesys, CancerVax, Genitope and others. There was one “kind of” successful company in Dendreon which gained approval for Provenge in 2010. Provenge was a dendritic cell vaccine for prostate cancer. In its phase 3 trials, it showed a meaningful survival advantage. However, the manufacturing process for Provenge was long, complicated and so costly that Dendreon could not turn a profit. There was an added problem in that Johnson& Johnson introduced Zytiga ,a new small molecule drug aimed at the same indication which provided a comparable survival benefit. As a result, Dendreon went bankrupt. These factors discouraged venture capital investment in dendritic cell cancer vaccines.

Northwest was an outsider to the club. As a result, it did not have research from Wall Street analysts and indeed the same factors that discouraged venture capitalists and investment banks concerned analysts. Also, on Wall Street research coverage for small companies is almost always tied to investment banking fees. Investment banking pays the salaries of analysts on Wall Street as the old business of paying firms commission for good recommendations disappeared as stock trading became a commodity. So, there has been no research coverage.

Northwest Has Been the Target of Extensive Stock Manipulation

For those of you who have followed my research, you will know that I believe that widespread manipulation of stock prices by investment banks and hedge funds (the wolfpack) using illegal naked shorting is commonplace on Wall Street. In the case of small, emerging biotechnology stocks the wolfpack has enormous power to control the price of a stock. I previously provided a link to the recent series of ten articles on illegal naked shorting for a detailed discussion of how this is done. Northwest came under the scope of the wolfpack in the 2013 period. This began with a series of articles from bloggers associated with Jim Cramer’s The Street.com attacking NWBO. They painted the company as having worthless technology and management as stock manipulators. With these blogs as cover, the wolfpack began a sustained attack on NWBO that has driven the stock to trade at pennies.

The stock actually traded quite well until the summer of 2014, not too much out of line with what one would expect for a biotech company with a promising new product in late stage trials. The Company had indicated that it expected that an interim analysis of the phase 3 trial would be done in mid-2014 and investors were anticipating that this would take place. Unexpectedly, the FDA mandated that enrollment in the phase 3 trial would be halted although patients already in the trial could continue to be treated. This halt was later lifted, but we still don’t know why it occurred. Management had previously guided that there would be an interim analysis of the trial. However, results of this interim analysis were never announced. The reason for the halt in enrollment has never been publicly explained although uncorroborated information that I have heard (but won’t discuss) suggests substantial malfeasance, but not by Northwest. Subsequently, the FDA allowed enrollment to be resumed and of course, the trial has completed and we will see topline data soon.

Length of Phase 3 Trial Has Fostered Doubt and Skepticism

The phase 3 trial of DCVax-L has faced hurdles that rival the odyssey of Odysseus. Indeed, its journey at twelve years has been even longer than the ten years of the odyssey. I am not aware of any other phase 3 clinical trial that has lasted this long as most run for one to five years. According to ClinTrials.gov the starting date for this study was December 2006. This has also been a significant cause of skepticism. So why the unprecedented delay?

There were two major reasons for this delay. The first was a lack of financial resources so that in the aftermath of the financial crisis of 2008 the trial was put on hold. A more important reason was that management made the conscious decision in the 2015 to 2016 period to not unblind the trial until it could determine if there was a survival tail. By this point in time, the medical community and biopharma industry had become aware based on experience with checkpoint inhibitors that a key characteristic of immunotherapies was that they produced extraordinary length of survival in a small, but medically meaningful percentage of patients; this came to be known as the survival tail. The original design of the phase 3 trial had designated progression free survival as the primary endpoint and overall survival as the secondary endpoint; these were accepted endpoints for chemotherapy drugs. However, management based on the survival tail thesis correctly decided that it needed to let the trial run longer in order to determine if there was a medically meaningful survival tail.

My Approach to Determining Stock Price Potential is Based on Comparison Valuations of Companies Importantly Based on T-cell Engineering

Here is my thinking on the potential price of NWBO if the phase 3 trial of DCVax-L is successful and the majority of investors come to the conclusion that DCVax-L will become part of standard of care for newly diagnosed glioblastoma. Right now, most investors are unaware of NWBO or are extremely skeptical. With success in the phase 3 trial, investor’s attitudes could turn to wild enthusiasm as is the case with the T-cell engineering companies. While the technologies of T-cell engineering and dendritic cell vaccines are biologically quite different, there are enough similarities to view T-cell engineering companies as comparables. If so, we can look to the valuations of these companies as a guide to the potential valuation that investors might place on NWBO.

My basic assertion is that Wall Street is totally off base in ignoring the potential of DCVax-L. It is not unprecedented that Wall Street can be dramatically wrong on a company or technology. Let me cite the case of Jazz Pharmaceuticals and Micromet. In 2007, I was doing consulting work for a company that was investing in Jazz. The situation looked hopeless as their lead product disappointed in a clinical trial and the company was in a desperate financial situation. The stock sold at $1.50 in June 2007. Under the brilliant leadership of Bruce Cozadd, the company refocused on a second product Xyrem, and maneuvered through the financial crisis. Today the stock is at $108.

Bispeciifc antibodies are one of the hottest research areas in biotechnology today. They are very competitive with T-cell engineered products in advanced cancers and virtually every major biopharma company has a development program. The first company to develop a bispecific antibody was Micromet. Again, I was doing consulting work for the same company that was investing in Micromet. Unfortunately, Micromet had a difficult time raising the great sums of capital needed to develop its products and elected to sell the Company to Amgen in 2012 for $1.2 billion. The market potential for bispecific antibodies will likely be in the several tens of billions of dollars. Had Micromet been able to get Wall Street’s backing, we would likely be looking at a company selling at a market valuations of perhaps $10, $20 billion or more.

As I said, there is no company that I am aware of that is developing the unique technology on which DCVax-L is based so I have chosen to look at the valuations of companies that are based on T-cell engineering such as CAR-T and TCR. Like DCVax-L, products being developed are based on living cells that evoke an immune response and their initial therapeutic target is difficult to treat cancers. Wall Street is all in on T-cell engineered products and their valuations provide a guide to what NWBO might sell for if investors embrace and become excited about dendritic cell cancer vaccines. Here are important comparisons between T-cell engineering companies and DCVax-L; most of which favor DCVax-L.

- T-cell engineering has been validated by the approval of Novartis’ Kymriah (2018) and Gilead’s Yescarta (2018) and Tecartis (just approved). There are no approved products based on dendritic cells and DCVax-L is the only product in late stage product in development to my knowledge.

- There is intense competition in the T-cell engineering space as there are dozens of emerging biotechnologies developing somewhat similar products. Three big pharmas- Novartis, Gilead and Bristol Myers Squibb- are also heavily involved. NWBO is the only company I am aware of that has a product in late stage development with a dendritic cell therapy. It is novel.

- The emerging biotechnology companies that I have identified in T-cell engineering are in an earlier stage of development than DCVax-L. To my knowledge, all of the products in development are at a phase 1 stage of development and have not started registrational trials. They are generally hoping to introduce new products in the 2022 and beyond period. DCVax-L could be commercialized in early 2021 if the phase 3 trial is successful.

- The T-cell engineering companies have been showered with cash by Wall Street. For example, Allogene will not begin a phase 1 clinical trial with its lead product until late 2021. It came public in 2019 and with that and follow-on offerings now has a cash balance of over $1 billion. Cash starved NWBO has a few million dollars, barely enough to get to phase 3 results.

- The three CAR-T products approved-Kymriah, Yescarta and Tecartis- are all targeted at advanced stages of cancer; i.e. patients who have previously failed several therapies. This is also true of the numerous other engineered T-cell products in development. DCVax-L is being investigated in the first line setting.

- Clinical trials for Kymriah, Yescarta and Tecartis were based on small trials involving 100 to 200 patients. The primary endpoint that led to approval was based on objective response rates (measurement of tumor shrinkage). Current trials planned by T-cell developed follow the same strategy. There was no data on survival although follow-ups to the trials suggests that 30% to 40% have extended survival. The DCVax-L trial is much better. in contrast is 311 patients with a control group and the most important information will be median overall survival and the shape of the survival tail. The data from the DCVax-L phase 3 trial will be more substantial and meaningful.

- The side effects of DCVax-L are remarkably mild. There can be injection site reactions and a mild transient fever that can be treated with Tylenol. In sharp contrast, T-cell engineered products are associated with grade 3 and 4 toxicities that can be life threatening. This is a major plus for DCVax-L.

- T-cell engineering is currently focused on treating hematological B-cell cancers, but will likely be effective in solid tumors. The technology on which DCVax-L is based is applicable to most solid tumors. Both have great pipeline potential.

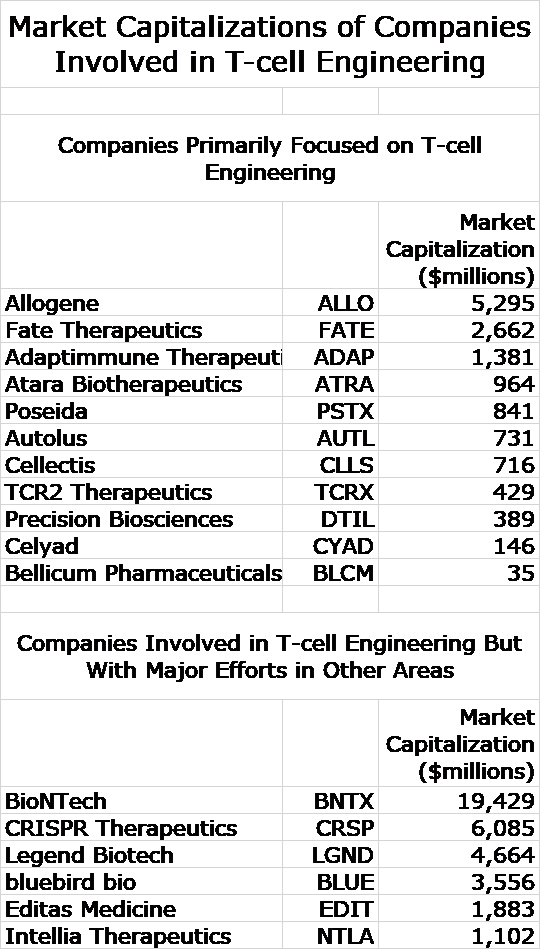

The following table shows the market capitalizations of 11 companies that are almost exclusively focused on T-cell engineering and six others that are heavily involved, but also have advanced development efforts in other areas. I submit that weighing all of these factors leads me to conclude that if the DCVax-L trial is successful and is viewed as being supportive of approval for the treatment of first line glioblastoma, that its valuation should be greater than most of the T-cell engineering companies. What do you think?

Allogene has a market capitalization of $5.3 billion even though it will not begin phase 1 trials on its lead product until late 2020. I think that investors are giving too much weight to the fact that its management founded Kite Pharma and sold it to Gilead for $12 billion. I consider its market capitalization excessive in a relative sense. It is my contention that NWBO because of its uniqueness and much later stage of development should probably be selling at a $2 billion or greater market capitalization. In my opinion, with an approval of DCVax-L and financing in place, we could be looking at a $6 to $9 billion market capitalization.

Tagged as DCVax-L Phase 3 Results, Northwest Biotherapeutics Inc. + Categorized as Company Reports, LinkedIn