Cryoport: This Unique Company is Poised for Explosive Sales Growth; Price Weakness is a Buying Opportunity (CYRX, Buy, $6.68)

Investment Thesis

By my analysis, Cryoport and its stock are coiled like a spring for future strong performance. My model is projecting over 50% per annum sales growth for the period 2017 to 2020 with sales estimated to increase from $12.1 million in 2017 to $41.8 million in 2020. The revenue mix is now shifting rapidly from providing cryogenic shipping services for products in clinical trials to commercial products that have much greater revenue potential for Cryoport. For example, the annual revenue potential for a product in phase 3 can be $200,000 to $1,000,000 and much less for products in phase 1 or phase 2. In late 2017, the first two CAR-T products supported by Cryoport were approved: these were Novartis’s Kymriah and Gilead’s Yescarta. Cryoport has guided that it believes that revenues from the initial indications could reach worldwide peak sales of $8 to $10 million. The expectation is that in the US peak sales will be reached in 18 months and that this will also be the case as they are progressively introduced in European and other countries where they should be approved in 2018.

I think that my sales projections through 2020 could be quite conservative (purposely so) for the following reasons:

- I do not estimate any revenue from other new products being commercially introduced by Cryoport clients. However, Cryoport believes that there could be two to four BLAs filed by its clients in 2018 and they are already discussing commercial launch strategies with several customers. It is difficult to predict the timing and indeed there is no guarantee of any approval. Hence, I am not assuming any revenues from new products in the 2017 to 2020 period even though I think there is a high probability for quite meaningful revenues.

- I do not include any additional potential revenues from new indications for Kymriah and Yescarta. Initially, Kymriah will be marketed for pediatric r/r ALL while Yescarta will initially only be marketed for r/r DLBCL. Management guidance for both of these indications is that peak worldwide revenues for Cryoport could reach $8 to $10 million. However, Novartis has just filed a supplemental BLA for r/r DLBCL (same indication as Yescarta) which will add additional revenues (not in my model) with sales beginning in 2018 in the US. Yescarta is in registrational trials in seven other types of leukemias/ lymphomas which have potential comparable to pediatric r/r ALL and r/r DLBCL. Novartis has not indicated that it is conducting similar studies, but it almost certainly is. I do not include any estimates for sales from new indications in my model. The revenue potential for each of these indications is of the same order of magnitude as those approved. I think that there is a high probability for quite meaningful revenues, but they are not included in my sales projections.

- Cryoport has given guidance that peak sales on Kymriah for r/r ALL in the US could be reached in 18 months and peak sales for Yescarta in r/r DLBCL in the US could be reached in the same time. However, I am assuming that peak sales in the US and other countries are reached in three years which is meant to be a conservative assumption.

- Cryoport is expanding into the logistics support of other types of products than CAR-T and regenerative medicines. For example, Bristol-Myers Squibb is expected to switch from an in-house cryogenic shipping solution to Cryoport for cell lines used in the manufacturing of an undisclosed monoclonal antibody product that has sales of over $1 billion. There are several other projects under way, which like the BMY example are essentially switching some aspects of logistics (not all) from the drug developer to Cryoport. I think we will likely see revenues from BMY in 2018, but this is not in my projections.

- Just recently, Cryoport announced that some of its customers asked it to provide shipping services for products that don’t require shipment at cryogenic temperatures of minus 238 degrees Fahrenheit. Many products are now shipped at 36 to 46 degrees Fahrenheit. Cryoport is really not broadly targeting this market, but some companies have requested that Cryoport get involved because they want access to its informatics for products shipped in this temperature range. There are no revenues for this in my projections.

Price Target Thinking

I have a 2020 price target of $20 for Cryoport. The Company is in an early stage of development in which revenues are a more predictable measure of value than earnings. As a company matures, the relevant measure becomes earnings, but for Cryoport this will likely be beyond 2020. Based on a comparison to emerging life sciences companies I think that Cryoport could be valued at 15 times 2020 revenues of $41.8 million. Based on 30 million fully diluted shares this would result in a market capitalization of $600 million and a per share price of $20+ in 2020.

Review of 3Q Results

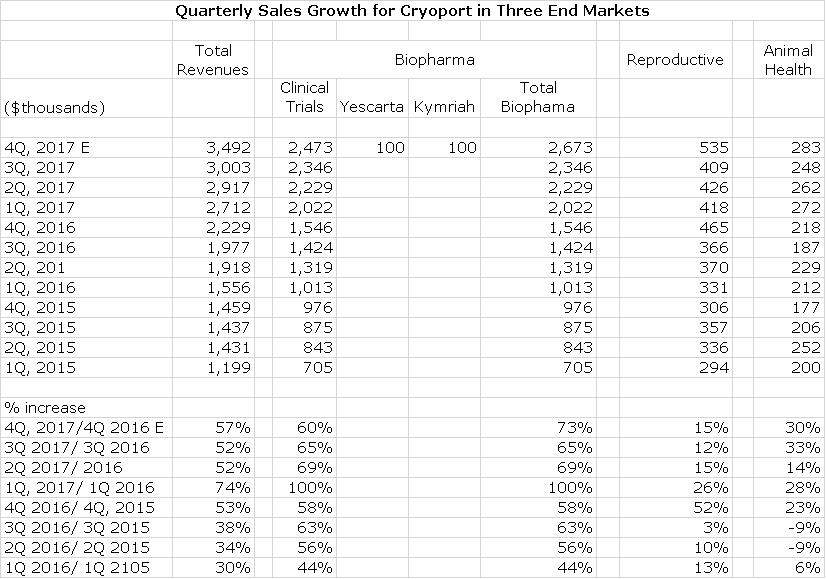

As expected, the third quarter continued to show very strong revenues trends that were in line with 2Q revenue increases. In the second quarter, sales increased 52% and in the 3Q 52%. There was nothing in the quarter of resultant conference call to change my extremely bullish view of the Company and stock. If you are not familiar with Cryoport, please review my initiation report of Cryoport: Initiating Coverage of this Highly Unique Health Care Company with a Buy (CYRX, Buy, $2.25). The following table shows quarterly sales trends for 2015 through 3Q, 2017 and my projections for 4Q, 2017 which illustrate the dramatic growth trends for that period.

Click to expand image

Clinical Trial Revenues, Historical and Projected

Cryoport is going through a major inflection point in its business as its clients begin to gain commercial approval of their drugs. You will notice in the prior table that for the first time, I am including revenues for the launch of Yescarta and Kymriah in my 4Q, 2017 projections. Clinical trial revenues in 3Q, 2017 were $2.3 million and came from 195 separate clinical trials supported by Cryoport. Company guidance for peak revenue potential for Yescarta and Kymriah in their approved indications is $8 to $10 million. However, approval for new indications could ultimately lead to peak revenues several times as large. In contrast, supported phase 3 trials can lead to $200,000 to $1,000,000 of revenues and phase 1 and 2 trials have even less potential.

The investment story is centered on commercial drug approvals, but in the time frame of 2018 to 2019, clinical trials remain important to total revenues. The past trend has been extremely impressive as is shown in the following table. Over the last eight quarters, sales have more than doubled and the number of clinical trials has more than tripled. A quandary for investors in 2018 and 2019 is what will be the rate of growth in those years?

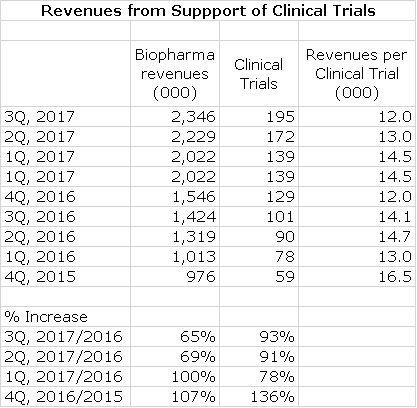

It is a difficult (nearly impossible) challenge to project with any precision the revenue trends for clinical trials. The mix between phase 1, 2 and 3 trials varies and is not known to investors. Also, predicting the change in number of trials supported is equally difficult. I have calculated the average revenues per trial in the following table which shows a variation from $16,500 to $12,000 over the last eight quarters, but this is a relatively meaningless figure. Ultimately, the projection of clinical trial revenues is a guess. I could make a strong argument that clinical trials in reproductive medicine are still in an early and explosive growth stage and that these trials are progressing from phase 1 to phase 2 to phase 3 with a major benefit to revenues. This could lead me to extrapolate clinical trial revenues at rates comparable or better than 71% in 2017 and 51% in 2016. However, because of the difficulty in predicting I am assuming a slowing in revenues to 40% in 2018, 30% in 2019 and 25% in 2020. Again, this is without much basis and is an effort to be conservative.

Annual Revenue Projections Through 2020

The next table summarizes my sales projections for the period 2017 to 2020. As previously explained, I have tried to be quite conservative in my projections.

My estimates indicate that Cryoport’s revenues will increase from $12.1 million in 2017 to $41.8 million in 2020. I have tried to be conservative in my forecasting. In the case of revenues from products in clinical trials, I have the rate of growth slowing from 71% in 2017 to 40%% in 2018, 30% in 2019 and 25% in 2020. I have no reason for projecting this sharp slowing, but the rate of growth is very hard to project and I want to be conservative. It is my sense that the growth of sales from products in clinical trials will be much stronger. My revenue projections for commercial products exclude some potentially important new sources of revenues as I discussed in detail in the investment thesis section of this report. Even with what I believe to be conservative assumptions I get explosive growth estimates.

Click to expand image

Why Has the Stock Been So Weak with Such Exceptional Growth Prospects?

Cryoport’s stock has been quite weak in recent weeks as the price declined from a high of $10.21 on September 22 to a current price of $6.68. Third quarter results were released after the close on Thursday November 3 and on Friday the stock declined steadily throughout the day from $7.58 to $6.68. The quarter was very strong and prospects for growth are exceptional as I have just discussed. There were no negative or cautionary comments on the call from management, indeed their tone was bullish. The three Wall Street analysts who cover the Company all commented that the quarterly results were impressive and reaffirmed their buys.

What is going on? This may partially have been due to profit taking after the incredible run-up in price this year, but this doesn’t explain the sharp price drop in my opinion. An important factor seems to have been a report from the small investment banking firm Maxim. They took the position that a small company called BioLife Solutions, on which they recently initiated coverage, has a superior dewar. Based on this, they projected major inroads into Cryoport’s business. The report is poorly reasoned and deeply flawed, in my opinion.

A Look at BioLife Solutions and the Maxim Report

Let’s take a quick look at BioLife. Its principal products are used to preserve cells that are the basis of manufacturing regenerative medicine products including CAR-T cells. Revenues from this business are running at a rate of about $8 million and based on a cursory look, there appears to be good potential for growth powered by the macro trends in regenerative medicine. This has similarities to market factors that drive Cryoport’s business. However, in cryogenic shipping solutions BioLife is a non-factor. Cryoport is currently supporting clinical trials for 23 of 28 CAR-T companies that I am aware of. It is supporting the commercial launches of the first two commercial products, Yescarta and Kymriah, from the two leading companies Kite and Novartis, as well as their clinical development program for these products. It also supports the clinical trials for the two other leading factors in CAR-T, Juno and bluebird bio. I carefully read the Maxim report and the regulatory filings of BioLife and I don’t think that the Company has only negligible, if any, sales from cryogenic shipping services and the Maxim report mentions only one CAR-T client in Japan. If this were a one mile horse race between Cryoport and BioLife Solutions, Cryoport would be at the half mile mark and BioLife Solutions would be searching for the starting gate.

BioLife ended the June quarter with $2.3 million of cash and the burn rate in each of the first two quarters of 2017 was $800,000. If this burn rate is ongong, the Company will have about $1.5 million of cash as of September 30, 2017 and would run out of cash at the end of the March 31, 2018 quarter. Obviously, the Company desperately needs to raise cash in the very near future. I have heard but cannot confirm that the Company may be planning an equity offering. If so, I think that Maxim should commit to not participating in the offering given the recently published bullish report that so fiercely attacked Cryoport. If they did participate, it could be interpreted by some as priming the pump for an offering which is certainly unethical and possibly worse. I would think that Maxim would not want to act in any way to justify these suspicions. Investors will watch this situation with great interest.

In this report, the analysts at Maxim represented that BioLife had a superior cryogenic service offering to Cryoport. The report focused on a comparison of the properties of the respective dewars and ignored the logistical, informatics software which has been so critical to Cryoport’s success; they barely touch on this. The discussion on dewars was very complex and I am not about to pass judgement on it. However, Cryoport management labeled the report a piece of fiction and went into a detailed critique of the note with highly detailed point by point rebuttals.

BioLife Solutions Faces Huge Completive Barriers in Challenging Cryoport

As the first mover in cryogenic shipping solutions, Cryoport has incredibly strong advantages. Here’s what drug manufacturer demands. What they want most of all is quality assurance, not the lowest shipping cost. Excursions in temperature during shipment can alter the characteristics of cell therapies and potentially affect patient outcomes or even ruin the product. Manufacturers want to be as certain as possible that the drug was maintained in the appropriate temperature range during shipment and if there is some issue going on during shipment that might threaten the integrity of the product, allow a response before the product is ruined. Kymriah is priced at $475,000 per treatment and Yescarta at $350,000. It seems unlikely that the potential for saving a small amount of money would be a reason to leave a trusted partner like Cryoport. BioLife would have to demonstrate superiority through a comparison clinical trial. This is not going to happen.

While the dewar is important in the Cryoport service offering, it must be combined with software that allows real time tracking of the product; Cryoport’s sophisticated software developed over the last five years allows this. Bear in mind that the three major shippers-FedEx, UPS and DHL- all have chosen to partner with Cryoport rather than develop their own cryogenic service offering. This indicates how difficult it would be for a startup company to compete against Cryoport.

Another important point to understand is that the Cryoport service is part of the BLA filing. If a manufacturers wanted to shift to a competitor it would have to amend the BLA filing which would take much time and effort and probably require clinical evidence that there is no effect on drug characteristics. No manufacturer is going to do this to save tens or hundreds of dollars on shipping costs. Along the same line, if a manufacturer uses Cryoport in the clinical trials leading up to a BLA filing, this becomes a critical part of the BLA. Changing to another cryogenic shipping system would require clinical data to show there is no effect on drug characteristics. Again, no manufacturer is going to do this.

I see the current base of supported clinical trials and any resultant commercial products as virtually impregnable to a potential competitor like BioLife. It will have to compete for new trials. However, with virtually no clients in the US and no track record, it is an unknown factor in cryogenic shipping. It will be difficult for BioLife to persuade companies to go with the unknown factor that they are. I repeat my previous metaphor that if this were a one mile horse race between Cryoport and BioLife Solutions, Cryoport would be at the half mile mark and BioLife Solutions would be searching for the starting gate.

Has Cryoport’s Stock Been Manipulated?

The sharp price decline has all the markings of a hedge fund hit job. Stock manipulation is a critical component of the business strategy for many (most) hedge funds who band together in wolfpacks. Illegal practices are extremely widespread to the extent that they target almost all small emerging companies at one time or another. Was this such a manipulation? It seems to walk like a duck and quack like a duck so there is a good chance that it is a duck (stock manipulation scheme). See my report Illegal Naked Short Selling Appears to Lie at the Heart of an Extensive Stock Manipulation Scheme

Regulatory authorities are either clueless (technologically over matched) or captured by the hedge funds so a Company under attack can’t count on them to thwart the wolfpack. The only real defense at this time is for a Company to perform. In the case of Cryoport, the fundamental outlook and growth potential should allow the stock to keep the wolfpack at bay and perform very well in coming years although I would expect periodic attacks like this that allow the wolfpack to stage highly profitable trades.

The Wolfpack is Omnipresent

Although this Maxim report is not to be taken seriously, I believe that it has been the pretense for an attack on the stock by a wolfpack of hedge funds using illegal naked shorting and high frequency trading to manipulate the stock price down. I am not alleging collusion between Maxim and the wolfpack as I have no way of knowing, but it certainly gave the wolfpack a pretense for their attack on the stock. The behavior of the stock on Friday November 3, 2017 as it declined 12% from $7.58 to $6.68 further confirms my belief that the wolfpack is attacking the stock. As previously mentioned, the 3Q results were very strong, the conference call was bullish and all three research analysts covering the stock reaffirmed their buys.

The stock steadily declined throughout the day as the wolfpack used naked shorting and high frequency trading to walk the stock down. One of the key strategies of the wolfpack is to make good news look bad. I have seen this strategy employed against tens or even hundreds of companies. The greatest threat from a wolfpack attack occurs if a Company needs to finance as the pack drives the stock down and forces financing at distressed levels. However, Cryoport has a very solid cash position and should soon become cash flow positive so that it will not need to use the capital markets for funding.

Tagged as Cryoport, Cryoport conference call, CYRX, third quarter of 2017 + Categorized as Company Reports, LinkedIn

Excellent article Larry. You read my mind and then addressed my concerns. I’ve come across Maxim in the past and have an extremely low opinion of the company. For those who didn’t listen to the call, the Maxim report was brought up by the first analyst during the Q&A phase of the call (likely pre-arranged). The CEO vehemently jumped all over the question and gave a very comprehensive answer.

One question I have for you Larry was about your statement that peak sales for Kymriah and Yescarta in the US will be reached in 18 months even though you are sticking to 36 months in your modeling. During the call, in answer to the Needham analyst’s question, Mark Sawicki (Chief Commercial Officer) seemed to state that a reasonable expectation would be a linear 3 year ramp to $8-10m in peak sales. Can you explain why you think it could be so much faster?

Finally, here is some fun with the numbers Cryoport provided in the presentation slides and in the past on the number of clinical trials it is supporting. From that data it seems that Cryoport has 195 of the total 934 clinical trials (21%) currently underway vs 9% of the 631 trials underway at year-end 2015. During that 21 month period it seems that Cryoport won 136 of the 303 net increase (45%) in studies, including 10 of the 16 increase in Phase 3 (62%) and of course both products approved for commercial sale.

Enjoyed your analysis. Excellent details. Cool company. One question. Is 15X revenue appropriate for a life sciences shipping company compared to other types of life sciences businesses? A standard high growth business might get 3-5X revenue.

Here is a sample of calculations of the ratio enterprise value to 2017 revenues (estimated) for a sampling of biotechnology companies; Amgen (5.2). Biogen (5.8). Alexion (7.8). Celgene (8.1). InCyte (13.9) and Seattle Genetics (20.2)