Repligen Has an Outstanding, Stable Business and Excellent Long Term Growth Potential (RGEN, Hold/ Buy, $14.07, Paid Subscribers Only)

Investment Background and Company Overview

I think that Repligen’s (RGEN) bioprocessing business is one of the best business models that I have seen in my many years as an analyst. Its products are used in the manufacturing of biologic drugs; they enjoy incredibly long life cycles because changing the manufacturing process for a biological product once it is approved or after it has completed phase III trials can change the characteristics of the product. Hence, a change in the manufacturing process at virtually any level can create troublesome regulatory issues as the FDA will require assurance that the product is unchanged. The agency may request new studies, possibly including clinical trials in humans that demonstrate that there is no change in the product.

The economic benefits of any improvement in manufacturing efficiencies are trivial in comparison to lost profits if output is interrupted by the need to validate a change in the biomanufacturing process or if in the worst case it changes the product characteristics. This means that once Repligen’s products are incorporated into a manufacturing operation at the clinical trial stage, they are almost certainly going to be used through the life of the product. As a result, its products enjoy very long life cycles and have minimal vulnerability to competition; Repligen’s products are like annuities.

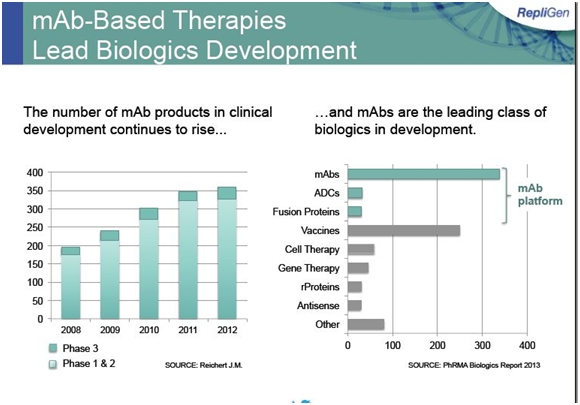

The foundation of its bioprocessing business is protein A, which is used to purify monoclonal antibodies during their manufacturing process. Repligen supplies over 98% of the world market for Protein A. The major macroeconomic force driving protein A sales is the clinical development and commercialization of biological products, especially drugs based on monoclonal antibodies. Monoclonal antibodies are a $57 billion global market growing at 8% or more per year; there are about 35 approved products and 350 new products in development. The projected 8% growth in sales for monoclonal antibodies is a proxy for future growth of Protein A sales. The following table shows the large number of monoclonal antibodies under development.

Protein A is 64% of Repligen’s bioprocessing sales and in order to achieve the faster growth of bioprocessing revenues as a whole of 10% to 15% which is management guidance, other areas must grow faster. These are the OPUS disposable chromatography columns and the growth factors businesses. Growth factors are about 20% of the bioprocessing business and can probably grow at 15% to 20% per year.

Growth factors is a solid opportunity for Repligen, but it is OPUS that can really be the dynamic factor for growth. OPUS is currently about 5% of sales and could increase by 75% in 2014. Longer term, Walter Herlihy, CEO of Repligen, has said that OPUS could reach the same level of sales as Protein A; he did not specify when this would happen. I have included a table at the end of this report that gives detailed revenue estimates for these product groups through 2019.

Investment Opinion

Looking at the Numbers

I continue to wrestle with the valuation of Repligen. The bioprocessing business is projected in 2014 to have $54 million of sales and EPS of $0.23 based on current products, I project organic five year growth for sales of 14% and 28% for EPS. I expect acquisitions to be made that can significantly increase the rate of increase of both sales and EPS.

Because of the very high quality of Repligen’s business, I would feel comfortable placing a 30x to 40x P/E on my 2014 projected bioprocessing EPS of $0.20. (Because of an already received milestone payment of $2 million, reported corporate EPS for 2014 are projected at $0.26). A 30x to 40 x P/E would result in a stock price of $6 to $8. However, the stock is selling at $14.00 or 66x projected 2014 EPS.

Another issue for Repligen is that I am projecting that EPS will drop from $0.51 in 2013 to $0.23 in 2014. Repligen through the end of 2013 was entitled to a royalty on Bristol-Myers Squibb’s blockbuster drug Orencia; this amounted to about $17 million of pretax income or roughly $0.40 per share in 2013. This royalty agreement expired at the end of 2013 and is responsible for the sharp drop in 2014. The best way of looking at the Company is to look at the projected trend in bioprocessing EPS as shown below:

You Just Can’t Look at EPS In Thinking About A Price Target

A valuation based solely on 2014 EPS projections however, fails to take into account other valuable assets of the Company. Repligen as I have explained in prior articles is a cash flow machine. Management has guided to a cash balance of $84 to $87 million by the end of 2014. This is $2.50 or more of cash per share. This cash position is different from that of emerging biotechnology companies which must consume all of their cash to fund operations. Repligen is a cash flow generating machine that generates cash flow that exceeds cash needed to fund operations. If Repligen were to choose to let cash accumulate on its balance sheet, I project that they would have $167 million of cash in 2019.

Repligen is not going to let cash accumulate on its balance sheet but will use it to increase shareholder value. If the $84 million of cash were to be given as a dividend, it increases the value of the stock by $2.50. If it were used to buy back shares at $14.00 per share, it would reduce the share count by 6.6 million shares or 20% of shares outstanding. A share buyback by reducing shares outstanding could increase the value of the stock from $6 to $8 which I suggested as fair value for the core business based only on EPS to $7 to $10.

Acquisitions Will Be Important to Future Growth

The examples of paying a cash dividend or buying back shares were only to demonstrate that the cash on the balance sheet has real value for shareholders, but cash is not going to be used in that way. Management has indicated that it will almost certainly use the cash to make acquisitions and has further indicated that it does not intend to do just small bolt on acquisitions with $1 to $3 million of sales, but strategic acquisitions in bioprocessing which I interpret as $10 million of sales or more.

To illustrate the potential impact on EPS of an acquisition, let me hypothesize what an acquisition might look like. Let’s assume that Repligen has the opportunity to buy a company or product with $10 million of sales and that it can buy this asset for cash at four times sales or $40 million. Let’s further assume that this business has gross profit margins of 50% like Repligen’s current bioprocessing business and that the asset can be manufactured in Repligen’s facilities and that the incremental marketing expense would be adding five salesmen which would cost about $1 million. With all of these assumptions, the operating profit contribution would be $4 million and the after-tax contribution would be $0.09 per share. This compares to my estimated 2014 EPS estimate for the bioprocessing business of $0.20.

With its 2013 year end cash position of $76 million and projected yearend cash of $86 million for 2014, Repligen is in the position to do one or possibly two acquisitions like this in 2014 or 2015. This could increase the bioprocessing EPS of the Company in 2014 from $0.20 to perhaps $0.29 with one acquisition and possibly $0.38 with two. Using a P/E of 30x to 40x and applying this to EPS of $0.29, results in a possible price range of $9 to $12 for the bioprocessing business; it would leave $40+ million on the balance sheet. This example assumes that Repligen pays cash but with its current price, it might also use stock.

With these assumptions, I think that it is reasonable to assume that the core bioprocessing business is worth $9 to $11. Some might argue that the promise of the bioprocessing business justifies an even higher P/E than 30 to 40. They might also argue that Repligen could be an extremely attractive takeover candidate so that it deserves a takeover premium. This could be but I don’t like to use heroic assumptions in my price target thinking so I am looking at the core business as being worth about $10.

Biotechnology Assets Add Still More Value

There is still another component of the business that stems from the Company’s heritage as a biotechnology company. As part of a strategic decision in 2012 to focus its efforts on the core bioprocessing business, Repligen out-licensed its therapeutic drug programs.

On December 28, 2012, it out-licensed to Pfizer (PFE) its spinal muscular atrophy (SMA) program, whose lead drug is RG3039, a small molecule drug candidate in clinical development for SMA. Pfizer will fund the clinical development needed to seek regulatory approval. Repligen is entitled to receive milestone payments and low single digit royalties on sales if the product is commercialized.

On January 21, 2014, Repligen out-licensed its histone deacetylase inhibitor (HDAC) portfolio, which includes the Friedreich’s ataxia program, to BioMarin Pharmaceuticals. Repligen received an upfront payment of $2 million in January 2014 from BioMarin (BMRN) and could potentially receive up to $160 million in future milestone payments. In addition, Repligen is eligible to receive royalties on sales of qualified products developed.

The clinical development program also included RG1068, a synthetic human hormone developed as a novel imaging agent for the improved detection of pancreatic duct abnormalities in combination with magnetic resonance imaging in patients with pancreatitis and potentially other pancreatic diseases. Repligen submitted an NDA to the FDA and a marketing authorization application to the European Medicines Agency in the first quarter of 2012. In the second quarter of 2012, it received a complete response letter from the FDA, indicating the need for additional clinical efficacy and safety trial data. It was also told by the FDA that it would need to do an additional trial. It is trying to find a partner for this program and will not spend any of its cash on future product development. This will be a very hard asset to partner and I think that it probably has no value.

The difficult question is what value to place on these biotechnology assets. For each $100 million of sales of licensed products, Repligen might be entitled to receive perhaps $10 million or royalties which would drop straight to the pretax income line. Taxed at a rate of 35%, each $100 million of revenues would result in $0.20 of EPS. Arbitrarily assuming sales of $200 million of licensed products in 2019 (for the sake of illustration), would result in $.40 of EPS. Placing a 30x P/E ratio on these EPS would suggest a stock price valuation of $12 in 2019 just from these products.

My Near Term and Long Term View

If we were to judge the value of Repligen only on the basis of projected bioprocessing EPS of $0.20 in 2014, the P/E ratio at 70 times seems overly high. Moreover, reported projected corporate (includes royalty income and bioprocessing) EPS are projected to decline from $0.50 in 2013 to $0.26 in 2014. I have argued at great length in the preceding sections that investors have to attribute value to the cash position and the biotechnology assets. However, the high P/E and the decline in reported EPS present a cosmetic issue. I have seen the Twitter critter day traders, not known for in-depth analysis, suggesting that the stock should be shorted.

I think that most sophisticated investors understand the value proposition of the cash position and the biotechnology assets. I don’t see much risk in the stock. However, to get the stock moving, I think that we need to see an acquisition (which is probable in 2014) or meaningful clinical data on the two licensed biotechnology drugs (not likely in 2014).

At this point, I am not aggressive on the stock. I need a catalyst like an exciting acquisition to get me fired up. I think that this is an exceptional company and will reward “buy and hold” investors handsomely over the next decade. My lukewarm stance on the stock should not be taken as a negative stance. Based on life experience, I think that when you are invested in a company like Repligen which offers exceptional stability and growth potential, you don’t trade in and out. The risk is that you get out and never get back in.

I own this stock and you couldn’t pry it out of my portfolio with a crowbar. I just don’t sell fundamental situations as strong as this. At the same time, I am reluctant to tell subscribers to initiate a position at this price and with what is now known about the Company. I would just urge you to keep this Company in mind and there should be an opportunity to buy the stock, usually there is.

Looking At Business Segments

Guidance for Company Results in 2014

On its conference call discussing 4Q, 2013 results, the Company provided guidance that bioprocessing revenues for 2014 will be between $52 and $55 million which is a 10% to 15% increase from 2013. In addition, it has already recorded $2 million from a BioMarin milestone payment in 1Q, 2014. The Company didn’t comment on potential acquisitions, but I think that there is a good possibility of a strategic acquisition with perhaps $10 million of sales.

Gross margins are expected to be approximately 53%, up from 51% in 2013; the longer term goal is to reach 55%. R&D expenses are projected to be $5 million and S, G&A to be $14 to $15 million. This should result in operating income of $10 to $12 million. The GAAP tax rate is estimated at 24% to 28%. This results in net income of $7 to $9 million. Based on the above, Repligen is expecting year-end cash of between $84 million and $87 million.

OPUS: Growth Potential Is Exciting

Repligen expects sales of OPUS Pre-Packed Columns to grow by 50% to 100% in 2014. It projects that a significant part of this increase will come from a new 45-centimeter diameter OPUS column that was launched in March. It has greater capacity than any competitive product on the market and was developed in response to requests from customers who are running larger fermentation processes that require larger columns for product purification.

Management cited three important recent developments for OPUS. First, it made the first sale of the 45 centimeter columns even before the formal commercial launch in March 2014. Second, it made the first sale of a set of process scale columns to a contract manufacturing organization working for a customer outside the United States and Europe. This supports the Company’s belief that in-country manufacturing in rest of world markets could increase the demand for the largest OPUS columns. Third, it made the first sale of process scale columns containing a Repligen proprietary Protein A media, which allowed the Company to capture the margin on both the OPUS column and the media packed inside. While these are early and singular examples, they exemplify some of the potential drivers of further growth of OPUS.

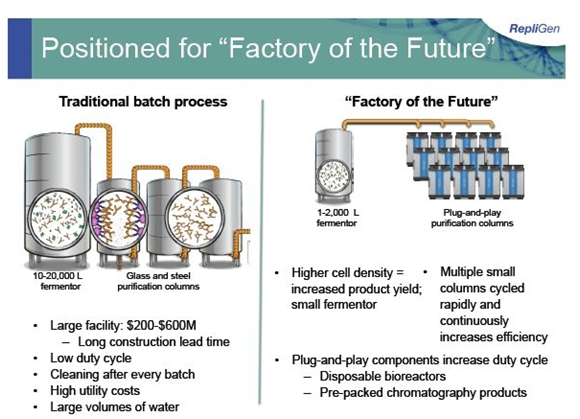

OPUS and the Flexible Factory of the Future

The manufacturing and purification of biological agents has traditionally been done in large dedicated, steel and glass facilities which run on a batch basis and lack flexibility. The goal of OPUS is to help create smaller more flexible factories of the future. OPUS is designed to be used as “plug-and-play” disposable plastic chromatography columns that are used in the downstream purification part of biopharmaceutical manufacturing processes. The columns are specially designed for each manufacturing process and can be packed with media of any type, not necessarily that using protein A.

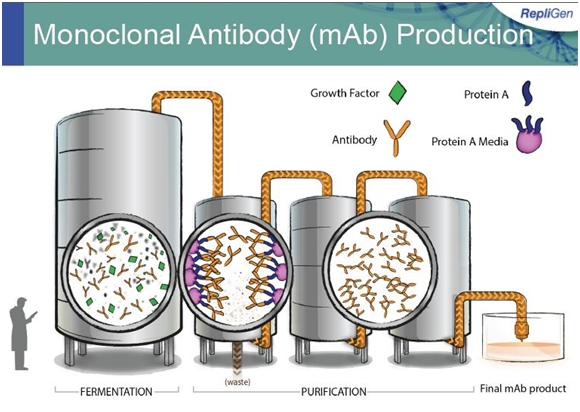

The next image shows a typical manufacturing facility and how Protein A and growth factors are used.

OPUS could change the current large manufacturing paradigm to more flexible factories of the future in which manufacturers can choose the media, column size and column bed height that is right for their process. Repligen manufactures these columns in a controlled environment and ships them by UPS to the manufacturer. The manufacturer can elect to either pack the column or have Repligen pre-pack the media. The value proposition of OPUS is that it improves manufacturing efficiencies and lowers costs by reducing time for column packing, validation, set-up and cleaning. The contrast between the old factories and Repligen’s vision of the factory of the future is visually depicted below:

The initial opportunity is primarily for products in clinical trials that have not yet finalized on a commercial manufacturing process. For a commercial product or a new product that has finished phase III clinical trials, a change to OPUS could be interpreted as a change in the manufacturing process that would have to be validated for the FDA. This could require a bridging study that would demonstrate that the manufactured product is equivalent or could possibly require a human trial. This is a major deterrent to adopting OPUS in these settings.

The original OPUS product offering, not surprisingly, is chromatography columns suitable for clinical trials and possibly commercial processes for low volume orphan drugs. Applications include a broad range of chromatographic separations and applications in biomanufacturing processes such as protein, peptide, and antibody separations; viral purifications and vaccine preparation; sample preparation; and scale-down model work, including validation studies.

OPUS sales will be driven by innovation and the company is most excited about its new 45-centimeter diameter OPUS column which has two to four times greater capacity than the largest disposable column size currently available. The development of this product was based on requests from customers who were running increasingly larger fermentations in their pilot plans that required larger purification columns.

The manufacturing of OPUS columns, particularly the large 45 centimeter columns require considerable manufacturing and materials expertise. Ordinary plastics are not strong enough and Repligen employs composite materials first developed by the aerospace industry. Also, the columns require exacting tolerance to maintain a uniform diameter along the length of the column.

The 45 cm columns are all pre-packed for the customer, either the end user or the contract manufacturer. Revenues depend on whether Repligen purchases the chromatography media for the columns or the customer supplies it. It is generally the case that Repligen purchases the customer’s choice of media and that cost is passed along to the customer at a small markup. If the customer purchases the chromatography media, there is a small packing charge. Revenues are much higher if Repligen purchases the media, but most of the profits in either case are due to the column. The 45 cm column sells for about $50,000 and has a gross profit margin of about 50%.

One of the important initiatives of Repligen is to develop their own media for some specialized applications. This would significantly improve the profits from a 45 cm pre-packed column but would not have much of an effect on revenues. Another research effort centers on multi-column chromatography and a number of customers are investigating this application. This is another effort aimed at increasing the purification potential. In particular, they are working with a large biopharma company on a research project that completes in mid-2014. This will point the direction for what the next steps should be. The goal is to extend the use of disposable columns from clinical to commercial stage. If this application takes off, they want to be the vendor of choice.

This will be a more competitive market than Protein A. The large manufacturers of chromatography media have limited offerings and a small European company is in the market. The strategy of Repligen is to offer the greatest diversity of columns and chromatography media. The large companies-GE, Millipore and Life- can only offer their own media. Repligen hopes to use its first mover advantage to become the dominant supplier. Also, the large companies are focused on the much larger sized media market. For them, Repligen may be a competitor in disposable columns but in terms of media can expand their media sales as a reseller.

Protein A

Repligen added two new types of Protein A affinity ligands in the last two years bring the total marketed to 7. All of these ligands are incorporated in media products sold by its partners. It is expected that these recently launched products will contribute incremental revenue of between $1 million and $2 million. Both have strong growth potential over the next few years and affirm our leadership in this business segment.

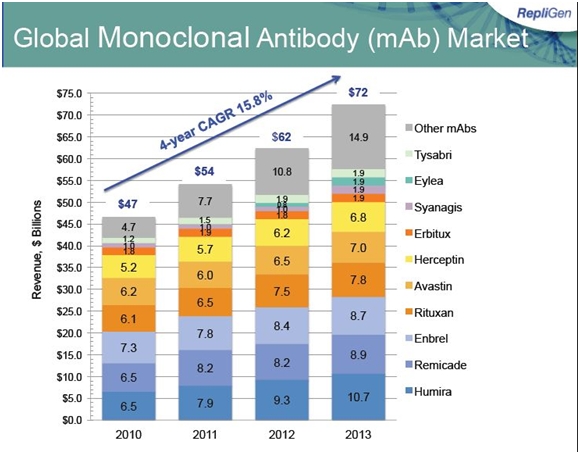

The biopharmaceutical industry as was previously mentioned has some 35 approved products based on monoclonal and 350 new products in development. Of particular interest are the anti-PCSK9 products of Amgen, Regeneron-Sanofi, Pfizer and Bristol-Myers Squibb. These products are targeting patients with high cholesterol levels who are resistant to statins; Sanofi has estimated this to be a market of 1 million patients. There is less confidence that the products will be used in the 17 million patient market currently treated by statins. This is a much larger market than rheumatoid arthritis market that accounts for much of the sales of Enbrel ($8.5 billion), Remicade ($8.7 billion) and Humira ($11.0 billion).

The second big major development effort by bio-pharma is in the checkpoint inhibitors; the anti-PD-1 inhibitors Bristol-Myers Squibb’s nivolimumab and Merck’s lambrolizumab. There are a board number of other checkpoint inhibitors under development. Analysts are pegging nivolimumab and lambrolizumab sales at $5 billion by 2020. The oncology markets addressed by the checkpoint inhibitors are much larger than those addressed by Rituxan ($7.6 billion), Avastin ($6.9 billion) Herceptin ($6.6 billion) and Erbitux ($1.9 billion).

The following table shows the current sales of the leading products based on monoclonal antibodies.

Growth Factors

The anti-PCSK9 drugs and the checkpoint inhibitors will also drive growth factor sales. Amgen and Repligen have a close relationship so that it is logical to speculate that the LONG R3 IGF-1 may be involved in Amgen’s anti-PCSK9 monoclonal. There are additional companies who are experimenting at fairly low volumes right now with IGF-1 in their development programs.

Repligen’s key growth factor product is LONG R3 IGF-1. The Company has been working with its distribution partner Sigma-Aldrich to increase use in the production of clinical materials for several mid- and late-stage clinical products. If one or more of these products is ultimately approved and successfully launched, it could significantly increase demand.

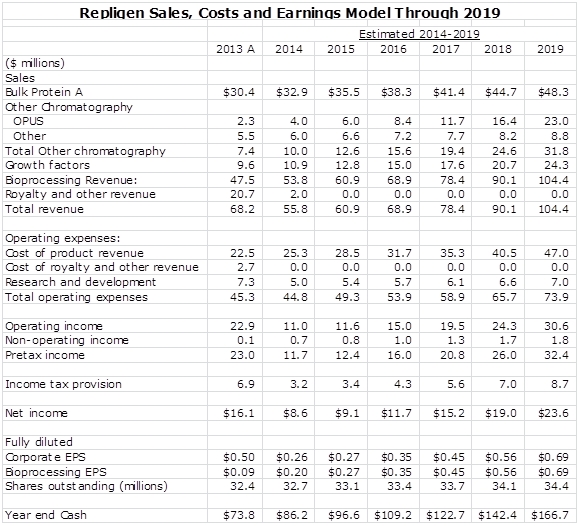

Detailed Income Statement Model

My detailed income statement model is shown below:

Tagged as Repligen, RGEN + Categorized as Company Reports