Comments on Agenus and Antares

SmithOnStocks Mailbox

About the Mailbox:

My mailbox comments are brief articles on stocks in which I am involved. These can come from recent events or from subscribers’ questions. They are meant to address specific issues about these stocks and are not full and balanced reports. Please refer to the Reports section of my website for more complete analyses.

Agenus: ASCO Selects Prophage Study for an Oral Presentation (AGEN, Buy, $6.94)

Investment Thesis

The ASCO Annual Meeting which will be held during May 29 to June 2 in Chicago is the most important conference of the year for presenting research findings in solid tumors. There are thousands of posters submitted by investigators for the conference and many are turned down. Of those selected most are designated as poster presentations in which the poster is pinned to a board for viewing by attendees. Poster presentations are made in a huge hall that can handle hundreds or even thousands of posters. During the course of ASCO there are several such presentations per day each involving hundreds or thousands of such posters. The scope of research is mind-boggling.

Only a select number of papers submitted to ASCO are selected for an oral presentation. Such selection signals that the research has some especially important findings. Hence the selection of a phase 2 study of Prophage for an oral presentation signals that ASCO believes the study to be highly significant. I believe that this selection has important implications for Prophage, Agenus and cancer vaccine therapy in general. From a stock market standpoint, some critics have stridently argued that cancer vaccines don’t work based on a number of failed development efforts in the past. They also argue that a phase 2 trial without an historical control doesn’t provide reliable information. This validation by ASCO negates both of these arguments.

This is very important for Agenus as most investors have written Prophage off and have valued Agenus primarily on the basis of its checkpoint modulators and QS-21 vaccine adjuvant. This puts Prophage back into the investment outlook almost as a new leg to the story. The recent strong move in the stock has been driven by news on its QS-21 vaccine adjuvant as used in Glaxo’s malaria and shingle vaccine. See the report and the report for more in-depth information. Prior to that, an important collaboration with Incyte on development of some of Agenus’s checkpoint inhibitors had given a big boost to the stock.

Agenus has previously indicated that it would put its resources behind the checkpoint modulators and search for a partner for Prophage. Many observers scoffed that they could find a partner, but this paper may make this more likely. If a partnership is consummated, it would be a huge boost for the stock. This paper suggests that Prophage as a single agent provided a very meaningful improvement over standard of care in treating newly diagnosed glioblastoma multiforme. Intriguingly, it suggests that combination with a PD-1 inhibitor like Merck’s Keytruda or Bristol-Myers Squibb’s Opdivo could produce truly dramatic results. This should make it easier for Agenus to find a partner for Prophage.

Prophage Presentation

The presentation, which is abstract #2011, is entitled “Newly diagnosed glioblastoma patients treated with an autologous heat shock protein peptide vaccine: PD-L1 expression and response to therapy, It will be presented during the Clinical Science Symposium at 8:48am CST by Orin Bloch, MD, Khatib Professor of Neurological Surgery and Assistant Professor of Neurological Surgery and Neurology at Northwestern University Feinberg School of Medicine.

Study Details

The Phase 2 study was single-arm trial that enrolled forty-six adult patients newly diagnosed with glioblastoma multiforme at eight centers in the U.S. Prophage was added to standard of care. Each patient received standard treatment of surgical resection followed by chemoradiation. Within five weeks of completing radiotherapy, patients received weekly Prophage injections for four weeks followed by monthly Prophage injections, and adjuvant temozolomide until the depletion of vaccine or tumor progression.

Study Findings

The primary endpoint of the trial was overall survival. Median progression-free survival in the trial was 17.8 months (95% CI, 11.3 – 21.6), and median overall survival was 23.8 months (95% CI, 19.8 – 30.2). This compares to a historical overall survival of 14.8 – 18.8 months for patients receiving standard of care alone. The vaccine was well-tolerated in the study with no severe adverse events attributed to the treatment.

Expression of PD-L1 has been shown to be elevated in patients with GBM, and each patient was also evaluated for PD-L1 expression as a predictor of survival. The median overall survival for patients with high PD-L1 expression (above the median, 54% of monocytes) was 18.0 months (95% CI, 10.0 – 23.3). Median overall survival for patients with low PD-L1 expression was 44.7 months (95% CI not calculable).

The finding on PD-L1 expression is important. Tumors express PD-L1 which interacts with the PD-1 receptors on T-cells and blunts the immune response to the tumor. The whole basis of the PD-1 inhibitors, Merck’s Keytruda and Bristol-Myers Squibb’s Opdivo, is to block the PD-1 receptor and prevent the PD-L1 secreted by the tumor from shutting down the immune response. These findings strongly suggest that Prophage results are significantly improved when PD-L1 is prevented from blunting the action of T-cells. It suggests that the combination of Prophage with Keytruda and Opdivo could dramatically improve the already impressive results seen with Prophage alone.

Antares (ATRS, Buy, $2.16)

Introduction

The quarterly conference call by Antares was in line with my recent comments on the Company. See my April 28 blog and my May 7 blog

Stock Opinion

I continue to be very positive on Antares. There are two critical drivers of the stock in 2015. The first is the approval and launch of an AB rated generic equivalent to EpiPen and the second is the trend in Otrexup prescriptions. I remain a buyer of the stock.

Approval of AB Rated Generic to EpiPen

Antares says that Teva is ordering Vibex injectors in anticipation of a launch. Antares is saying publicly that they expect the launch in 2H, 2015, but are not more specific. I think they may be hoping for an approval and launch before August.

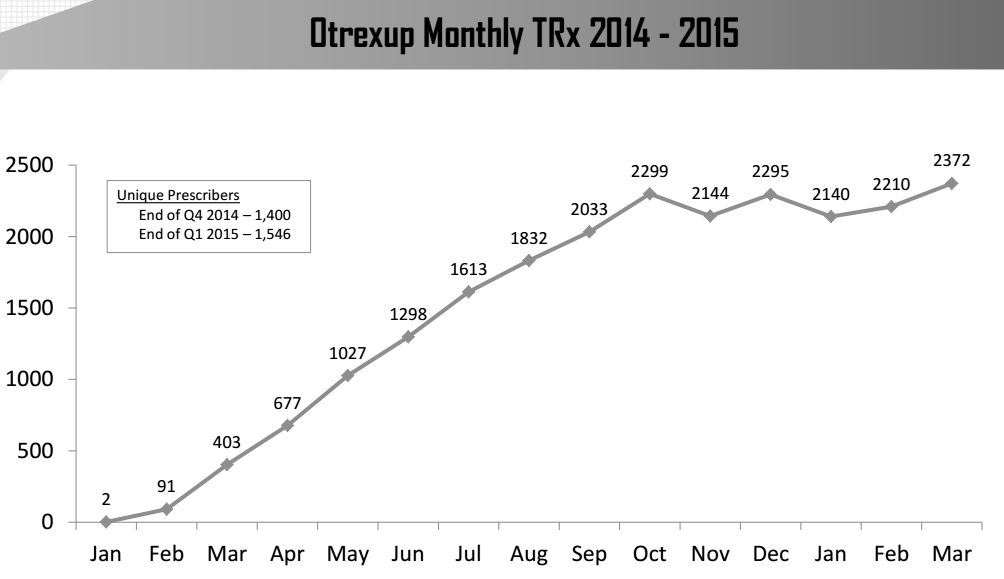

Prescription Trends for Otrexup

As with most products launched in biopharm, Antares has been frustrated by hurdles set up by managed care. The most important of these has been the requirement for prior authorization. In addition, because rheumatoid arthritis is a slowly progressing disease so new medicines are gradually worked into the physician’s armamentarium. The Company probably underestimated this effect.

In addition and as I have previously discussed, sales force disruption and competition from Medac slowed the launch. The sales force uncertainty resulted from the decision to bring management of the sales force under the direct control of Antares; it had previously been managed by the contract sales organization Quintiles. The Company retained 19 of 28 older reps and hired 13 new reps. This created some disruption in productivity as reps were wondering if they would be retained. There was also a very heavy sampling program for Rasuvo that had an effect.

Total prescriptions for Otrexup peaked in October of 2014 at 2,299 and were largely flat or down from October levels in November, December, January and February. There was an uptick in March as total prescriptions achieved their best total ever of 2,372 total prescriptions which was 3% above October total prescriptions and 6% above the average for November, December January and February. This is shown in the following table.

Otrexup Projections

I am estimating that April prescriptions increased about 7% although the final numbers have not been released. Antares reported on the call that in the latest week in May, total prescriptions were the highest ever reached. I think that the maturing of the sales force and measures taken to help physicians overcome managed care should result in good sequential sales. The situation with Rasuvo is harder to judge, but I think the market is of sufficient size that it can support two products.

My first quarter sales estimate for Otrexup was $3.16 million and actual sales were $3.00 million. This is the first time that my quarterly sales estimate was close to actual sales and not too high. My quarterly sales projections for Otrexup are 2Q ($3.7 million), 2Q ($4.5 million) and 4Q ($5.6 million). This would bring full year sales to $16.8 million. Management has stated that Otrexup would be profitable at sales levels in the $22 to $24 million range. My 2016 sales estimate is $36.9 million so that if I am correct Otrexup should be a solid profit contributor in 2016.

Some Upcoming Events to Put on Your Calendar

Agenus: R&D Day May 14, 4:30 PM EST

Derma Sciences: May; CMS decision on whether to reinstate Medihoney reimbursement

Discovery Laboratories: Phase 2a enrollment is completed, could see results in May. The key to look for are signals of efficacy

Kite R&D Day June 23, 2015

Kite: Presentation at UBS, May 18, 8:30 Am EST

NeoStem Presentation at Marcum Conference, May 28, 8:30 Am EST

Neuralstem Annual Meeting June 19

OncoSec Medical Presentation at Marcum Conference May 27, 1:00 PM

Tagged as AGEN, Agenus, Antares, ATRS, EpiPen, otrexup, Prophage + Categorized as Smith On Stocks Blog

Larry:

On Feb. 14th 2014 you wrote 2 small paragraphs that began: “I am also just beginning to do work on NeoStem…”

Since then there’s been nothing, until today, just above in SOME UPCOMING EVENTS: “NeoStem Presentation at Marcum Conference, May 28, 8:30 Am EST”

Have I missed something? A report perhaps? As a deeply underwater NBS shareholder, I’d be happy to read a report by you on this company. -L.

Thank you Larry for staying on top of these 2 companies and the others you follow….

Thank you for answering my questions about NWBO in a previous post….

With all the advancements that are being made in immunotherapy, do you think NWB0 is still near the lead, or are we falling behind everyday?

Yes, AF and other writers are getting into my head as I await some “new” news out of NWBO, besides, “stay tuned”…..I am long AGEN and ATRS and several others you have recommended….

I sure hope NWBO is 1/2 as good as I thought it was a year ago when we thought we would be seeing some data on “L” and “D” ….. Waiting and hoping, long…..thanks and thank you for your opinions on these and the other companies you follow….cheers.