Repligen: A Buy and Hold Stock: OPUS Promises to be a Dynamic New Product (RGEN; $9.87)

Report Summary

In this report, I go through a detailed sales, earnings and cash flow projections for the period 2013 through 2019. I am projecting that sales of the core bioprocessing business will grow at 13% per annum in the 2013 to 2016 timeframe. The EPS picture is complicated because the expiration of the royalty paid by Bristol-Myers (BMY) to Repligen (RGEN) on the $1 billion blockbuster Orencia; this will contribute about $18 million to 2013 results and nothing in 2014. It will reduce year over year EPS by about $0.37 per share. Because of this I am expecting EPS to decline from an estimated $0.49 in 2013 to $0.25 in 2014 on a fully diluted shares basis. In 2015 and 2016, I am projecting EPS of $0.31 and $0.39 which represent increases of 24% and 25% respectively.

The period of 2013 to 2016 has reasonable visibility for forecasting given the predictable and recurring sales characteristics of the Company’s product line. Beyond that there is more uncertainty and greater potential for error, but I believe that the rate of EPS growth can accelerate in the 2016 to 2019 period due to a new product line of disposable plastic chromatography columns called OPUS. There is a good deal of excitement in bioprocessing manufacturing circles that the factory of the future will use “OPUS-like” products to replace the steel columns now being used. In the last quarter conference call, Repligen’s CEO Walter Herlihy said that OPUS has the potential to be as large as protein A for the Company, but he did not specify in what time frame this might occur.

OPUS is now in the beginning stage of its product roll out as sales started on a modest scale in early 2012. It will take manufacturers several years to evaluate OPUS, first in clinical trials for their new products and then taking it forward into commercialization. For reasons explained in more detail later in this report, OPUS is only likely to be used in new products and not those that are commercialized or have gone through phase III trials. I think that OPUS could be a strong contributor to sales and earnings in the 2017 and beyond period. Based on the prospects for OPUS, I think that operating results could accelerate in the 2016 through 2019 period with sales growing at 18% per year and EPS growing at 31%. OPUS adds a dynamic new element to the long term Repligen investment story from the time that I initiated coverage nine months ago.

Price Target Thinking

In arriving at a one year price target for Repligen, my methodology starts with estimating the P/E ratio that investors one year from now (third quarter of 2014) will place on EPS projected for the core bioprocessing business in 2015. I then use a sum of the parts analysis to take into account free cash on the balance sheet and the value of biotechnology assets that are being partnered to arrive at a price target. Repligen should not be valued on EPS alone.

The first question to consider is what multiple should be placed on 2014 and 2015 EPS of $0.25 and $0.31 respectively. Based on the recent stock price of $10.00, the P/E ratio for 2014 is 40 and for 2015 is 26. This does not seem to be a bargain P/E ratio but it is not outrageous if my EPS growth rate projections of 24% and 25% in 2015 and 2016 and 31% in the 2016 to 2019 time frame are reasonably accurate.

However, there is also value in Repligen beyond that afforded to the earnings power of the bioprocessing business. By yearend 2014 the cash per share of Repligen is projected to be $2.37 and as I have pointed out, not much of this is needed for operations so it represents real value to shareholders. Repligen also has three biotechnology assets that it is monetizing. Two of these are orphan drugs that could have very significant potential. It is very hard to estimate the value of these assets. However, as a rough stab I think that if these assets were the basis of a standalone biotechnology company, based on the valuations of comparators, they might be valued at $50 million or $1.55 per share. This exercise suggests that cash on the balance sheet and the biotechnology assets are worth about $4.00 per share. If so this means that investors are paying just $6.00 for the core bioprocessing business. The 2014 and 2015 P/E ratios based on projected EPS of the bioprocessing business and the recent price of $10.00 are 24.0 and 19.0.

My one year price target for Repligen starts with applying a P/E ratio to projected 2015 EPS. I think that based on the prospect for 24% or greater EPS growth for the next six years, it is not a stretch to apply a P/E of 29 to the core EPS of $0.31 in 2015 which would produce a stock price of $9.00. Adding in the value of the biotechnology assets and cash of $4.00 produces a one year price target of $13.00. I also think that there is room for upside surprise in my EPS estimates if the Company uses its cash to make a meaningful acquisition.

The thing that most concerns me with my price target is that Repligen is not well covered by Street analysts at this point in time. There is only one Street analyst and myself covering the Company. As a result, investors might not be aware of the complexities of the investment scenario and could become alarmed by the sharp drop in EPS that is inevitable in 2014 and what appears at first glance to be the very high valuation on earnings. This has the potential to initially cause concern with the stock and have a negative effect on the stock price. I am willing to assume this risk and consider any weakness as a buying opportunity. This is a classic “buy and hold” story in my opinion.

Investment Overview

Repligen (RGEN) has gone through a metamorphosis that has dramatically changed its business model and investment outlook. For many years, it was focused on drug development but it was also quietly building a high quality bioprocessing business that provides consumable products used in the manufacturing of biological products. The acquisition of its major competitor, Novozymes (now Repligen Sweden) in 2011 provided the critical mass for a standalone business in bioprocessing; management and the board decided to exit the drug development business to focus on bioprocessing.

I think that Repligen has one of the best business models that I have seen in my many years as an analyst. Products used in bioprocessing have very long product lives because changing the manufacturing process for a biological product once it is approved or after it has completed phase III trials can change the characteristics of the product. Hence, a change in the manufacturing process at virtually any level can create troublesome regulatory issues as the FDA will require assurance that the product is unchanged. The agency may request new studies, possibly including clinical trials in humans, that demonstrate that there is no change in the product. The economic benefits of any change in manufacturing efficiencies are trivial in comparison to lost profits if output is interrupted by the need to validate a change in the biomanufacturing process.

This means that once Repligen’s products are incorporated into a manufacturing operation at the commercial level they are likely to be used through the life of the product. As a result, its products enjoy very long life cycles and have minimal vulnerability to competition; Repligen’s products are like annuities. I have written two previous reports on the Company and if I have sparked your interest in Repligen, I suggest that you read those reports. They explain in more detail the products of Repligen and the business environment in which it operates.

About 67% of 2013 product sales will come from sales of protein A and I estimate that Repligen has over 95% of this market. Protein A is used in the production of almost all products that are based on monoclonal antibodies Monoclonal antibodies are a $57 billion global product category that is growing at 9% or more per year; there are about 35 approved products and it is an area of intensive research interest as there are estimated to be 350 new products in development. Six of the ten best selling drugs in the world in 2012 were monoclonal antibodies and included Enbrel, Remicade, Rituxan and Avastin. Monoclonal antibodies sales are responsible for 33% of the $160 billion global biologics market.

The cornerstone of my original positive investment thesis was built on the estimate that protein A sales could grow at 9% per year or more in line with the growth of sales of monoclonal antibodies as a class and as I just discussed, that its products would be used through the life of the drugs in which it is incorporated in the commercial manufacturing process. In addition to protein A, there are two other product groups; these are other chromatography products (an estimated 17% of 2013 sales) and growth factors (20%).

I had looked at the two other components of the business as being support players to protein A with slightly better growth prospects in part due to the potential for acquisitions. However, in the nine months since I initiated coverage of Repligen, it has become apparent that the Company has another major product prospect with its OPUS disposable chromatography columns. The OPUS line was launched in February of 2012 and could account for 5% of revenues in 2013.

Sales and Earnings Model: 2013-2019

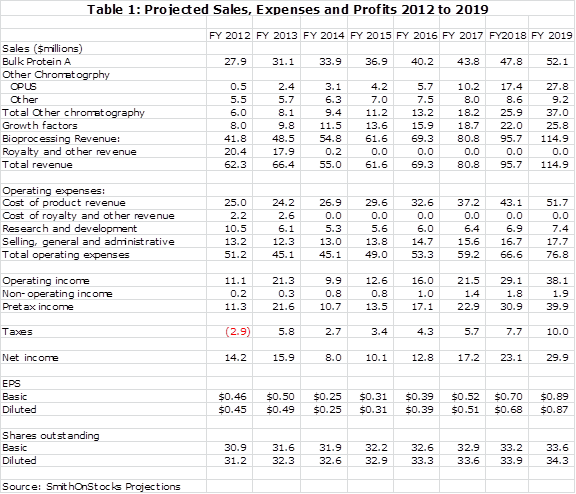

One spreadsheet is worth a thousand words. Table 1 shows more graphically than I can describe the projected sales, expenses and profits for Repligen. On the sales line, it projects bulk protein A as growing at about 9% per year consistently through 2019. While protein A sales will remain a dominant product, I show it declining from 65% of bioprocessing sales in 2013 to 58% in 2016 and 45% in 2019. I am looking for the other chromatography products category (which includes OPUS) to grow at 17% per year in the 2013 to 2016 time frame and accelerate to 41% per annum growth over the 2016 to 2019 time frame. I am projecting about 17% per annum increases in growth factors over the 2013 to 2019 time frame.

In looking at the following table, you can see a line item entitled royalty and other revenue that declines from about $18 million in 2013 to virtually nothing in 2014. Through its drug development efforts Repligen holds a patent that Bristol-Myers Squibb (BMY) licensed for the development of its large selling anti-inflammatory drug Orencia, which has current sales of over $1 billion. This licensing arrangement expires at the end of 2013 with the result that Orencia royalties will drop from $18 million in 2013 to nothing in 2014. Beyond 2014, the company will derive all revenues and profits from bioprocessing.

With its exit from drug delivery, Repligen dramatically changed its cost structure. It slashed R&D expenditures by more than half and realized operating efficiencies arising from the Novozymes acquisition. The new business structure will not need intensive investment in R&D and S, G & A which I am expecting to increase at 7% and 6.5% per annum. This lower rate of spending relative to the projected sales growth rate is what provides the operating leverage that leads to the 24% and 25% increases in EPS in 2015 and 2016 and even faster growth beyond then. Modest improvement is expected for gross margin and that can also contribute earnings leverage. The sales and earnings summary is as follows:

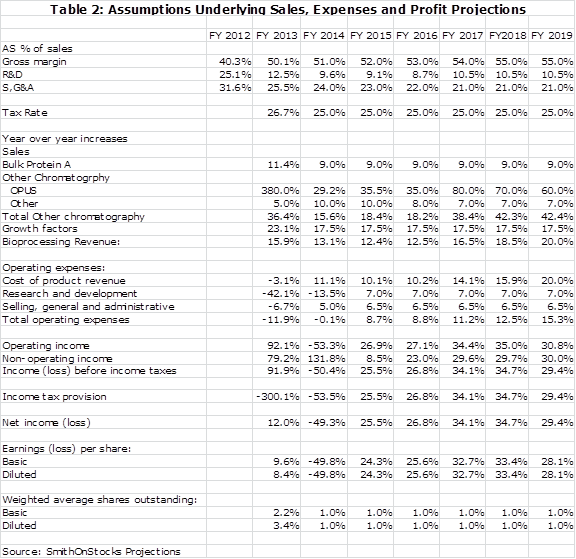

Key assumptions that underlie the sales and earnings model are shown below in table 2:

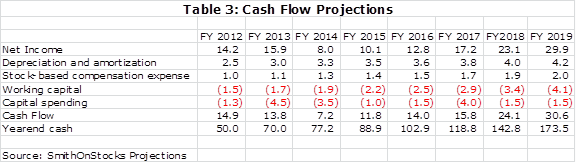

There is another aspect of Repligen that is just as important to consider as sales and EPS growth and that is cash flow generation. The bioprocessing business is not capital intensive and I expect a significant buildup in cash. In the biotechnology business from which the Company sprang, cash on the balance sheet is usually destined to be consumed by the burn rate and has little value for shareholders beyond that. The cash on Repligen’s balance sheet does have value as it can be used for acquisitions or possibly to be returned to shareholders through dividends or stock repurchases. Table 3 shows my cash flow and yearend cash projections for the Company.

I think that Repligen will use its cash to make acquisitions that could substantially change the projections and should increase the rate of sales and earnings growth. Management has given loose guidance that it could make one product or company acquisition per year. There is always risk in making acquisitions, but management so far has shown great expertise with the Novozymes and OPUS acquisitions. Hopefully, they can continue to make good acquisitions.

How OPUS Was Developed

Beyond the update on sales, earnings and cash flow and the discussion of my price target, the other major objective of this report is to focus on OPUS, which is very important to my longer term projections. Repligen acquired patented technology from BioFlash Partners which was combined with internal research to develop the OPUS (Open Platform User Specified) product line. The business goal was to develop a line of disposable chromatography columns that could increase the speed and efficiency of production and decrease overall biomanufacturing cost through fully disposable downstream processing.

BioFlash was founded in 2006 on the premise that biomanufacturing would shift from permanent glass and steel production facilities to ones that used disposable products. Its technology was originally developed by Dyax in the late 1990s. BioFlash was formed in 2006 based on an exclusive worldwide license to this Dyax technology. Repligen was an early venture capital investor in BioFlash. It then acquired patented technology from BioFlash Partners on March 3, 2010 obtained as a purchase of assets. The terms of the acquisition included an upfront payment of $1.8 million, a contingent milestone and royalties based on product sales.

The OPUS Product Line

OPUS is designed to be used as “plug-and-play” disposable plastic chromatography columns that are used in the downstream purification part of biopharmaceutical manufacturing processes. The columns are specially designed for each manufacturing process and can be packed with media of any type, not necessarily that using protein A.

Manufacturers can choose the media, column size and column bed height that is right for their process. Repligen manufactures these columns in a controlled environment and ships them by UPS to the manufacturer. The manufacturer can elect to either pack the column or have Repligen pre-pack the media. The value proposition of OPUS is that it improves manufacturing efficiencies and lowers costs by reducing time for column packing, validation, set-up and cleaning.

The initial opportunity is primarily for products in clinical trials that have not yet finalized on a commercial manufacturing process. For a commercial product or a new product that has finished phase III clinical trials, a change to OPUS could be interpreted as a change in the manufacturing process that would have to be validated for the FDA. This could require a bridging study that would demonstrate that the manufactured product is equivalent or could possibly require a human trial. This is a major deterrent to adopting OPUS in these settings.

The original OPUS product offering, not surprisingly, is chromatography columns suitable for clinical trials and possibly commercial processes for low volume orphan drugs. Applications include a broad range of chromatographic separations and applications in biomanufacturing processes such as protein, peptide, and antibody separations; viral purifications and vaccine preparation; sample preparation; and scale-down model work, including validation studies.

OPUS Launch

Repligen launched its initial process or research scale OPUS in February of 2012. It is a new way of thinking about purification and manufacturing operations that are traditionally slow to implement change. An evaluation involves numerous people in manufacturing, processing, quality control, regulatory and finance to all sign off. In some cases, there may be embedded costs due to existing facilities that are a barrier to change. The normal evaluation period for companies that are contemplating bringing a new bioprocessing product into their GMP manufacturing suite is about one year. As they hit that one year point, Repligen began to see a significant uptake in orders and customers in 1Q, 2013.

The OPUS introduction has been encouraging and management has estimated that it could contribute 5% of product sales in 2013 or about $2.4 million. The Company believes that this is a disruptive technology and has significant growth potential with new applications and new customers arising steadily. Management believes that it will be a key driver of sales in 2016 and beyond and sales eventually could become as large as those of protein A.

OPUS Pricing and Economics

OPUS provides a significant opportunity for Repligen to increase the value added of its purification product line offering beyond protein A. For a given chromatography column application, for every $1.00 of sales produced from the sale of protein A, there might $5.00 or more potential by attaching the protein A to the chromatography beads and another $0.50 if the medi is pre-packed in a column. Repligen is now in a position to capture a larger part of $6.50 commanded by the packed column instead of just $1.00 from protein A.

The customer can choose to pack the media or have Repligen pack it. Prices vary widely by the product being manufactured, but in a representative example, the value of the column might be $35,000 and the media might be $50,000 producing $85,000 of revenue for the pre-packed columns. The media is supplied by one of the big three media suppliers so that Repligen is a re-seller that receives small margins. The margin on the disposable column might be 55% while the margin on the media could be 5%. The economics for Repligen clearly relate to the disposable column.

During the 2Q, 2013 conference call, CEO Walter Herlihy said that the Company is now working on a project that could result in the sale of 100 columns per year; he didn’t specify when this might take effect if the customer goes ahead, but it is probably not a 2014 event. He also didn’t say if the contract would involve packing the column or just selling the column itself. In the case of just selling the product, it would be a $3.5 million sales opportunity that could produce $1.9 million of gross profits. If the columns were pre-packed, revenues could be $8.5 million with gross profits of $2.2 million. This would be an annuity that would occur every year as long as the product is manufactured. The 100 columns represent a high end opportunity as an average contract might be 50 columns per year.

Market Opportunity for OPUS

OPUS is a disruptive technology so that it is difficult to judge the market potential. For background, the worldwide market for chromatography resins for both commercial and clinical use is estimated to be $500 to $750 million. There are no estimates on the market size of chromatography columns as they are generally embedded in the cost of a manufacturing facility. Repligen believes that the market for pre-packed media in disposable columns for clinical trials and low volume orphan drugs is currently about $100 million. However, as use expands into commercial products and new applications arise, I suspect that market potential will expand very significantly.

OPUS Growth Drivers

One of the emerging opportunities for OPUS is the use of multiple disposable columns to replace one large steel column. One disposable column can be removed at a time and replaced so that there is no need to periodically shut the process down, clean the column and then repack it. With multi-columns run in parallel, the process can be made to run continually instead of on a batch basis. A value added component of OPUS is that the column is just disposed of and does not have to be cleaned.

These are early days and many potential customers are in a test phase or are just watching from the sidelines. Repligen has about about 5 to 10 customers who are repeat users as most potential customers are in an evaluation phase. There is one orphan drug that is being manufactured commercially with OPUS at this time. Seven of the top ten biomanufacturing companies are evaluating multi-columns.

The use of multi-column arrays was an initiates in 2013 with OPUS and this will be joined by another promising new product initiative in 2014. The multi-array columns allow continuous purification during the fermentation run. Repligen can pack the columns in an array that that would be ready for the customer to snap into the pumping stations and tubing sets. This provides a plug and play purification solution that provides the same continuous purification during the fermentation cycle.

Customer feedback indicated that the increasing scale of disposable fermentation facilities now being adopted require larger disposable purification capacity. In response to this Repligen has developed columns with two to four times greater capacity which it plans to launch in early 2014.

This is a new opportunity separate from multi-columns allowing OPUS can to address larger purification needs. Larger columns will have a width of 45 to 60 centimeters versus the currently marketed 10 to 30 centimeter columns.

The use of arrays and larger columns gives Repligen the opportunity to move into commercial biomanufacturing processes in the future. This has much greater potential than the clinical trial and orphan drug markets that will be the focus in the 2013 to 2016 time frame. At the moment, there are only a few large companies that are first movers with this idea. However, Repligen firmly believes that this is the factory of the future and is actively working with these vanguard companies.

OPUS Competition

The question arises as to whether Repligen is now competing with its large protein A customers and if this could strain their relationship. GE and Life Technologies do sell products which compete with OPUS. However, I do not see this as a problem. They sell some pre-packed disposable columns, but their primary interest is to sell chromatography media. In its OPUS products, Repligen is buying the media with protein A attached from GE and other manufacturers and packing it into their specially designed columns. I think that these companies view Repligen as a re-seller that can expand demand for their chromatography media product lines.

There is only one small company competitor and that is Atoll, a privately held European company. Their columns aren’t as large. There is a question on their balance sheet and their ability to stay around unlike Repligen which has a history and a strong balance sheet. Manufacturers can’t take a chance on a small company going out of business and this is currently a disadvantage for Atoll.

OPUS Manufacturing

Repligen is expanding capacity so that it will have two clean room facilities dedicated to OPUS. These will have the capacity to produce 500 columns per year. Assuming a cost per column of $35,000 this expansion can support $17.5 million of sales. This gives an insight into the optimism of management as OPUS sales in 2013 are projected to come in at $2.4 million. The clean rooms should be operational in 4Q, 2013.

OPUS Intellectual Property

To protect the investment in OPUS technology, Repligen has filed a patent application on the current OPUS column design and expects there will be additional intellectual property associated with the larger size columns now in development.

Growth Factors: The Third Business Line

Through the Novozymes acquisition, Repligen acquired fermentation growth factor products that are essential for proliferation and maintenance of cell lines used in the manufacturing of cell based therapies such as stem cells, monoclonal antibodies and recombinant DNA products. Growth factors, like chromatography products, are a fast growing component of bioprocessing. It is estimated by Repligen that the current market size is $50 million to $100 million. This gives Repligen a foothold which it plans to expand through internal development and acquisition.

The most important product is LONG R3 IGF-I which is one hundred times as potent as recombinant insulin and native IGF, which are currently the most widely used growth promotants. It is sold under a distribution agreement with Sigma-Aldridge which extends to 2021 and is now used in nine commercial biopharmaceutical products. Key customers include Amgen , Roche, and Chugai The other growth promotant products acquired were long epidermal growth factor (LONG EGF), transforming growth factor alpha (LONG TGF-α), and recombinant transferrin (r-Transferrin) which is as an iron supplement for cell culture and supplements for serum-free or low serum cultures.

The growth factors business is different from OPUS in that OPUS is driven by continual innovation while growth factors is more reliant on sales reps differentiating Repligen offerings from other products. Like OPUS, customers are unlikely to replace existing growth factors used in a commercial process or a product that has completed phase III trials for fear that this might have an unpredictable effect on the end product. Hence, the marketing focus is to get manufacturers to adopt products in the pre-phase III stage of developing the process. Like OPUS, once a customer adopts growth factors they are likely to be used through the life of the product.

Demand is driven by new customers and by products moving from clinical to commercialization and increases as unit volume of the products grows. Management believes that the growth factors business can grow in excess of 15% annually.

Tagged as Bristol-Meyers (BMY), OPUS, Orencia, Repligen, RGEN + Categorized as Company Reports