Derma Sciences: Close to Upgrading (DSCI, $4.54)

Investment Perspective

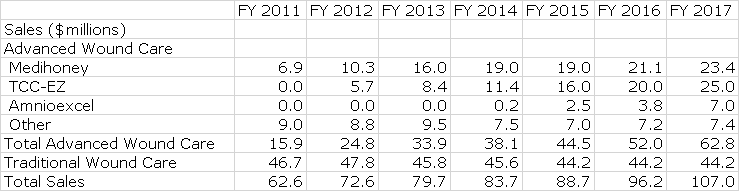

With the failure of its biotechnology drug candidate aclerastide, Derma Sciences is abandoning drug development efforts. The Company has also signaled that it will slowly be phasing out of its Traditional Would Care (TWC) business which is based on commodity products including compression products, adhesive strips, impregnated dressings, wound closure and gauze. It will now focus on its Advanced Wound Care (AWC) business which markets innovative and differentiated products through a Company owned 50 representative sales force. In 2015, I estimate AWC sales of $44.7 million and TWC sales of $44.2 million.

The AWC business is much more profitable with gross margins of about 48% versus 26% for TWC. Investors should essentially look at AWC as the basis for investment. I am projecting annual sales growth rates for AWC in 2015, 2016 and 2017 of 17%, 16% and 20% respectively. Derma Sciences made a huge bet on aclerastide that unfortunately did not pay off. I estimate that the Company spent about $55 million on this venture. Management has been and will continue to be criticized for moving so aggressively into biotechnology drug development with which it had no experience. In retrospect what’s done is done and it is unproductive to weigh in on this.

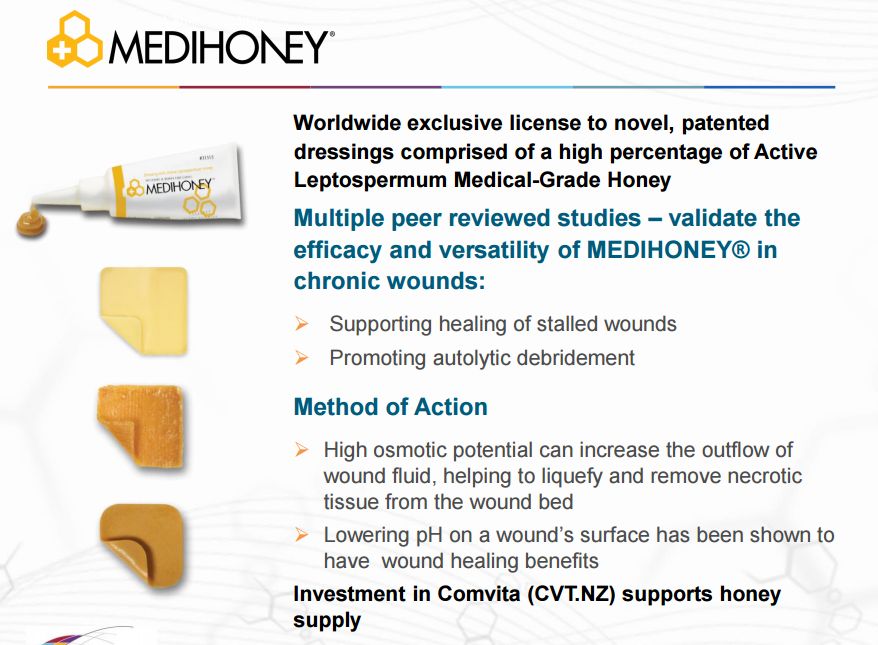

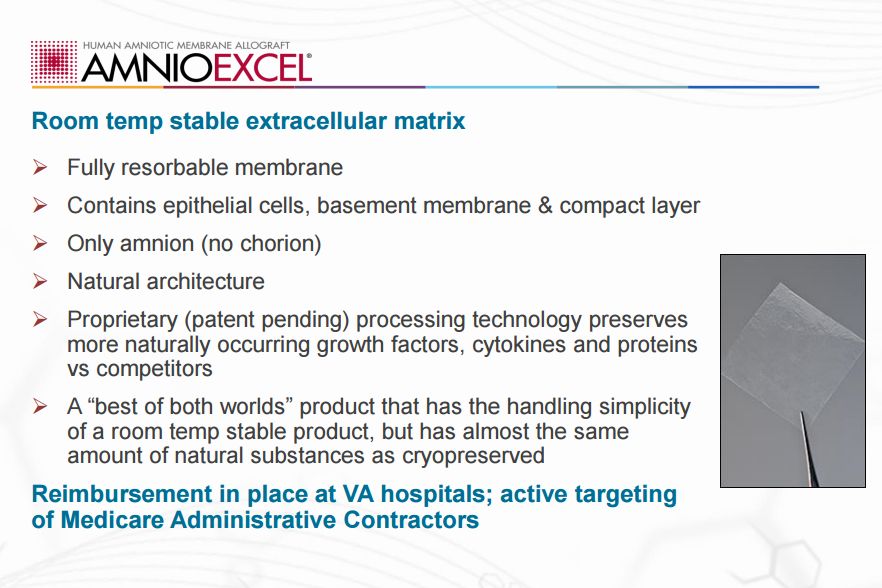

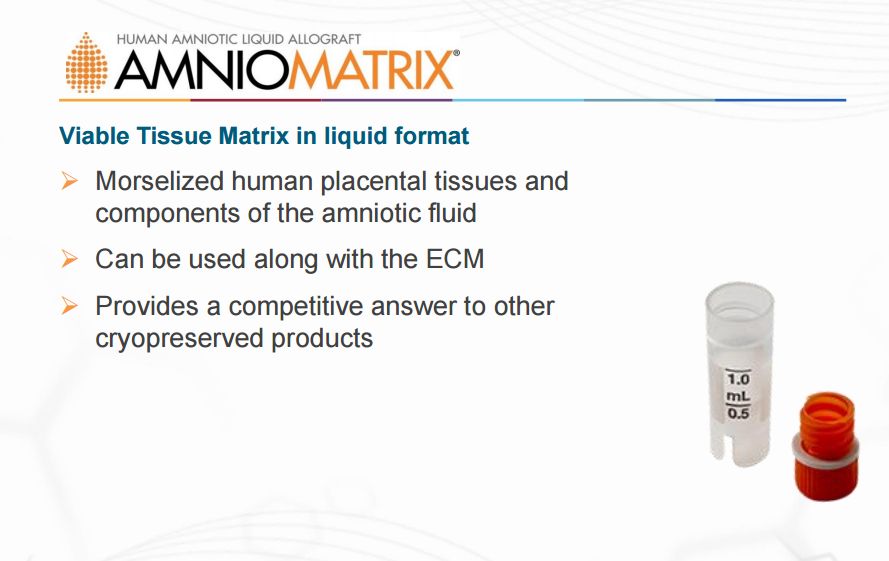

Investors focused on aclerastide miss the exceptional job that management has done in building the Advanced Wound Care business. In parallel with the drug development effort, Derma invested in acquiring proprietary products for Advanced Wound Care and building a direct sales force which I regard as a very important asset. The three key products of AWC are Medihoney wound dressings; AmnioExcel and AmnioMatrix (placental tissue) wound dressings; and TCC-EZ cast for diabetic foot ulcers. These were each acquired on very reasonable terms and then further developed by Derma. I think that the direct sales force and these three products form a solid foundation for growth.

AWC sales grew at 56% in 2012 and 37% in 2013. Reimbursement issues with TCC-EZ in 2014 slowed sales growth to 12% in 2014. In 2015, TCC-EZ regained adequate reimbursement and increased sales by 40% in 2015, but Medihoney sales were flat due to Medicare reimbursement cuts. I project that AWC sales will increase 17% in 2015. Looking forward, TCC-EZ should continue to show strong growth while management projects Medihoney sales will increase about 11% to 12% per year. The Amnio placental tissue wound care products are probably the most exciting growth prospect for the Company but they are in a launch phase and sales are still small. It is based on these three products that I am projecting annual sales growth rates for AWC in 2015, 2016 and 2017 of 17%, 16% and 20% respectively. It is possible/probable that acquisitions of other products could accelerate this growth.

Building the AWC sales infrastructure and investing in aclerastide resulted in a loss of $29 million through the first nine months of 2015. The cash burn was about $8 to $ 9 million per quarter so that the cash balance was reduced from $75 million at the beginning of the year to $49 million at the end of the third quarter. Of the $26 million of cash burn so far this year aclerastide may have accounted for half of this ($13 million) and the remaining business the other $13 million. There will be some expenses associated with wrapping up the aclerastide trials but this should be out of the picture by the end of 2015. Management has given no guidance on yearend 2015 cash but let’s assume that the 4Q, 2015 burn rate will be $8 million like the first three quarters. If so, the cash position going into 2016 will be $40 million.

The Company has given guidance that it can achieve cash flow breakeven with $91 to $92 million of sales from its wound care business and that it will reach breakeven cash flow in 3Q, 2015 and report profits on a GAAP basis soon thereafter, say 4Q, 2016 or 1Q, 2017. I estimate that the Company will roughly burn through about $7 million in the first nine months of 2016 so that when it reaches breakeven cash flow in 3Q, 2016 it could have a reasonable cash position of about $33 million, give or take. If so, I do not expect the Company to be in a position where it is forced to raise cash at a distressed stock price and going forward it may not need to raise any cash.

I project that in 2016 AWC sales could amount to $52 million that are growing at somewhere between 15% and 20%. TWC could be about $44 million of sales with 0±2% sales growth. The aggregate business would be cash flow positive and begin to report profits in 2017. There would be enormous profit leverage going forward as much of the infrastructure costs would be fixed and sales force productivity should be building. This makes for an interesting growth situation.

How does one value DSCI? We can’t really look at EPS in the 2016 period and probably not in the 2017 period so that the level of sales and growth rate of sales will determine the stock price. Based on my sales projection for AWC in 2017 of $62 million and the current market capitalization of $111 million, DSCI is selling at 1.8 times 2017 sales of AWC products, which are my total focus on the Company. There is no ready company that we can look to as a peer company to DSCI. However, if we were to consider it to be a specialty pharma company, the multiple placed on AWC sales would likely be in a range of 2.5 on the low end to 4.5 on the high end. This would result in a potential price range of $6.00 to $11.00 in 2017.

Based on this analysis, DSCI looks to have meaningful upside over a two year period. However, I think that management is in the penalty box right now due to the aclerastide failure and also because it did not see the slowing in sales of AWC in 2014 and again in 2015. I think that investors will be cautious on the Company until they get a better fix on the cash situation and gain confidence that management’s positive guidance on the AWC business is being realized. When management misses on guidance as it has for two years in a row, investors will be in a “show me you really have a handle on your business” mode. I am more aggressive. I believe that DSCI will be a rewarding investment over the next two years and I am recommending purchase.

To help you put my comments in perspective, I have included my estimates for key products and product groups of the Company. DSCI only breaks out sales of Advanced Wound Care and Traditional Wound Care in its regulatory filings; other numbers are my estimates. I have included sales estimates for Traditional Wound Care products in 2016 and 2017 even though part or all this product line could be sold by then. I would also suspect that the Company will acquire one or more new product lines for AWC by then which could be in part financed by sales of TWC products. The following estimates do not (cannot) take these dynamics into account.

CEO Ed Quilty’s Comments on the Business

I listened to Mr. Quilty’s comments at the Piper Jaffray conference in December 2, 2015. The format of the meeting was a fireside chat with attendees. This article is based on notes that I took

Slowly Exiting Traditional Wound Care

Derma may be slowly existing Traditional Wound Care and its commodity wound healing products to focus on its differentiated Advanced Wound Care products. The company has invested heavily is building a sales organization to support the AWC products. With this new strategy, the Company is predicting that it will become cash flow positive in 3Q, 2016 based on achieving annual sales run rate of $91 to $92 million for both TWC AND AWC; profitability should follow shortly thereafter. The Traditional Wound Care business is based on commodity products and is all about price. Large chunks of the business stem from private label manufacturing contracts. In 2014 they lost a significant contract and in 2015 they gained a contract. Overall sales prospects for TWC with all of this is essentially 0% ± 2%.

TCC-EZ

When the product was acquired in 2012 sales were a little over $3 million. It will do a little over $16 million in 2015 and perhaps $20 million or better in 2016. It only has a 3% share of the diabetic foot ulcer market so there appears to be a lot of room to grow. They now have a patient data base that will allow them to go to payors to talk about how cost effective TCC-EZ can be. There is a solid reason to suggest that it should be a therapy of choice for early stage diabetic foot ulcers. It could reasonably achieve sales of $50 million in a few years according to Mr. Quilty.

TCC-EZ is arguably the best available treatment for early stage diabetic foot ulcers. When used correctly on appropriate (early stage) patients it can achieve a very impressive 89% healing rate. In an era in which we have seen drug treatments with much lower rates of effectiveness sell at tens of thousands of dollars per year, the cost of TCC-EZ is $100 per treatment. Sales in 2015 have shown very significant increase of 40%.

Medihoney

Medihoney since 2008 has been covered by CMS under CPT codes. In early 2015, a CMS medical director issued a clarification about surgical dressings containing therapeutic agents like medical honey; this move seemed to be directly targeted at Medihoney. This meant that the product essentially lost Medicare reimbursement so that as of January 31, 2015, all of their Medicare business disappeared. In 2014, sales of Medihoney were about $19 million and about $4.0 million came from Medicare which all went away. In 2015, sales of Medihoney were flat at $19 million as Medicare losses were offset by growth in sales to nursing homes and hospitals.

Derma has been trying very hard to regain Medicare reimbursement, but success is uncertain. Mr. Quilty sees Medihoney as growing at 10% to 15% without success in regaining Medicare reimbursement and in this case sales of $35 to $40 million dollars could be reached in coming years. If they are successful in getting CPT codes back, there could be a substantial acceleration of growth over and above the 10% to 15%.

Physicians have a lot of choices for wound dressings and Medihoney is not used on every wound. Derma has established themselves as the Medihoney Company and Medihoney is a strong brand in the wound healing community. They have a significant advantage in that their New Zealand partner called Comvita, a $100 million company, is the biggest harvester of manuka honey in the world. Comvita controls a good proportion of manuka honey production in New Zealand. Derma has rights to all medicinal applications of this honey. All honeys are not the same and manuka honey has properties that make it perfect for wound dressings as it has anti-microbial, anti-inflammatory and debridement properties.

They also have two strong patents around the way they use the honey. Anyone who makes a dressing that is comprised on more than 50% of any type of honey would be in violation of one patent. This patent has been defended successfully. The other patent is around the gelling agents that they use to stabilize the honey in the substrate in which they deliver it.

AmnioExcel and AmnioMatrix Placental Tissue Products

Diabetics can be difficult to treat for foot ulcers as they often have neuropathies so that they do not even feel the wound on the bottom of their foot. This may mean that by the time they know they have a problem and see a doctor their ulcer is seriously advanced. Placental allografts like Amnioexcel are used primarily when other treatments have failed or the wound is too advanced for them to be effective and there is concern that the foot will have to be amputated. The mortality rate for patients who have foot amputations is about 50% within four years. There are 80,000 of these amputations each year. Placental tissue products have proven effective at putting off amputations. It is not a pleasant treatment. Patients have to go in a hospital or wound center and have the bottom of the foot scraped and possibly rescraped several times to get the treatment to take.

Derma wants to be a company that can offer an effective treatment at every stage of diabetic foot ulcers. These are extensions of the other treatments they are offering. If the doctor needs this type of product, they have it.

Amnioexcel and AmnioMatrix are in the words of Mr. Quilty “like all competitive products is placental tissue”. The leading company in this area is MiMedX and the next leading company is Osiris. Derma lags far behind these market leaders and cannot aspire to challenge their positions. The strategy is to gain a small but meaningful segment of the market. Key to this strategy is gaining broad reimbursement and demonstrating efficacy through clinical trials. By the end of 2016, Mr. Quilty expects that all seven regional Medicare carriers will reimburse Amnioexcel XL; this should lead to a sharp upward inflection in sales in 2017.

Sales in 2015 are expected to approach $2.5 million of sales. In an unspecified period, Mr. Quilty thinks that sales can reach $20 to $25 million of sales. Gross margins on this product are about 72% as compared to the current AWC gross margin of about 48%.

The Sales and Marketing Infrastructure

They have 50 sale territories (50 reps) in the US that are managed by five regional managers. They have five TCC specialists who support each of the regions, a clinical nurse in each of the five regions. There are three corporate account managers who call on managed care and group purchasing organizations. They are in all of the major purchasing groups. The Company will continue to add more sales reps but they are very expensive. Generally sales reps begin to pay for themselves in about one year. They will more as they can afford them, but won’t add any more reps until they reach cash flow breakeven.

The main focus of the marketing infrastructure is to call on the 1300 to 1400 wound clinics in the US. These wound centers are like the quarterbacks of wound care for not only patients at these centers but also those who go to hospitals and are in nursing homes. The wound center doctors also practice in hospitals and nursing homes.

Acquisitions

DSCI is actively looking at new product acquisitions. One of the key criteria has to be that the product is already on the market and that they can fit it into their marketing infrastructure. Products must have sales and have positive cash flow with margins that make them immediately accretive. They have several products that they are looking at right now.

Tagged as AmniMatrix, Amnioexcel, Derma Sciences, DSCI, Medihoney, TCC-EZ + Categorized as Company Reports